Using Data-Driven Insights for Optimal Debt Collection Strategies

Using Data-Driven Insights for Optimal Debt Collection Strategies

Using Data-Driven Insights for Optimal Debt Collection Strategies

Using Data-Driven Insights for Optimal Debt Collection Strategies

Anant Sharma

Anant Sharma

Anant Sharma

Debt collection is becoming more complex, with rising delinquencies and evolving consumer behaviors. Traditional collection methods often rely on outdated assumptions, leading to inefficiencies, missed opportunities, and strained customer relationships.

The solution? Data-driven insights for better debt recovery. By using customer data—such as payment history, demographics, and behavioral patterns—you can identify high-risk accounts early, tailor collection strategies, and improve recovery rates.

The need for smarter debt collection is growing rapidly. The market for AI-driven debt recovery solutions is projected to surge from USD 3.34 billion in 2024 to USD 15.9 billion by 2034, reflecting a CAGR of 16.90%. This growth underscores the increasing reliance on data analytics, AI, and automation to optimize collections.

In this guide, we’ll break down how to implement data-driven strategies for debt collection, ensuring higher recovery rates, better decision-making, and smarter resource allocation. Let’s dive in.

What Are Data-Driven Insights for Debt Collection?

Debt collection has long been a challenge, with traditional methods often leading to poor recovery rates, high operational costs, and frustrated customers. If you’re relying on generic collection strategies, you might struggle with low response rates, ineffective communication, and wasted resources. That’s where data-driven insights change the game.

Data-driven insights help you move from a reactive to a strategic approach by using real-time data to understand debtor behavior, predict repayment likelihood, and tailor collection efforts. Instead of sending the same reminders to every debtor, you can use intelligent, personalized strategies that improve engagement and increase recovery rates.

Importance of Data-Driven Insights in Debt Collection

A data-driven approach allows businesses to make informed decisions, optimize resources, and improve recovery rates. By utilising data analytics, you can predict payment behaviors, segment customers effectively, and refine communication strategies. Below are the core importance that enhance the efficiency of debt collection efforts.

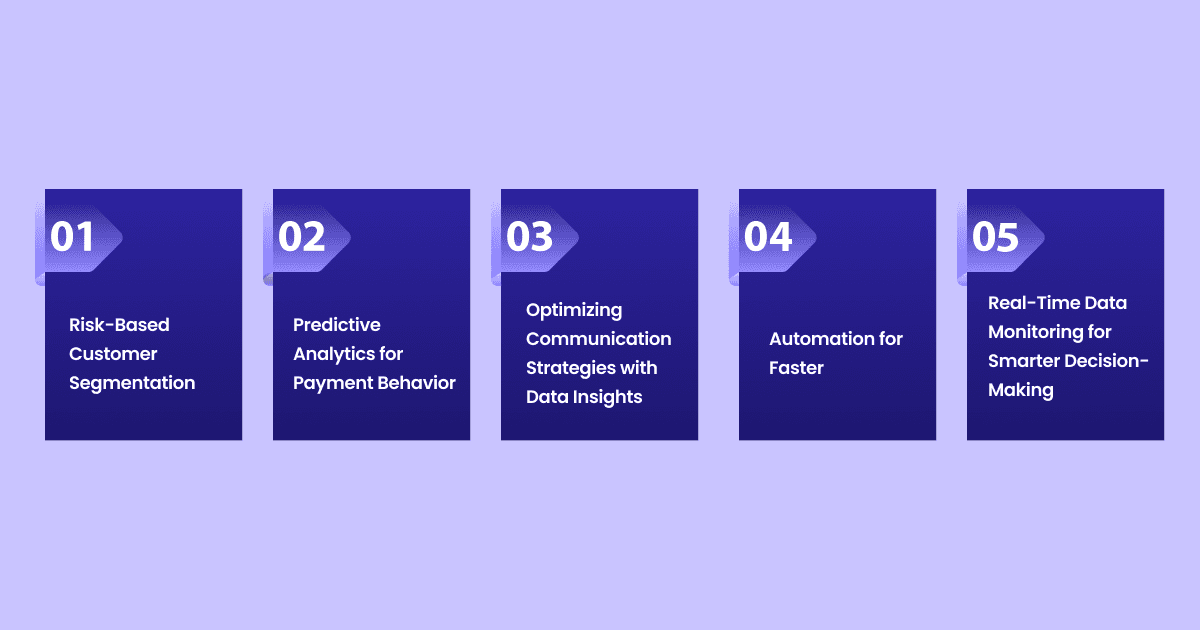

1. Risk-Based Customer Segmentation

Not all customers who miss payments are the same. Some face temporary financial challenges, while others have a history of defaults. To ensure effective debt collection, businesses need to segment customers based on risk levels using historical data, credit scores, and repayment patterns.

How It Helps:

Prioritization of Collection Efforts: High-risk customers with frequent missed payments or declining credit scores require proactive intervention through personalized repayment plans.

Customized Payment Plans: Medium-risk customers may benefit from flexible settlement options, reducing the likelihood of complete default.

Lower Operational Costs: By allocating resources efficiently, collection teams avoid wasting time on low-risk customers who typically resolve their debts with minimal reminders.

Rifa’s advanced analytics automatically segment customers based on real-time data, identifying high-risk accounts early. This allows businesses to apply targeted strategies, reducing the chances of default while improving recovery rates.

2. Predictive Analytics for Payment Behavior

Predictive analytics enables businesses to anticipate which accounts are likely to default and which customers may need early intervention. This involves analyzing key factors such as:

Payment history – Late payments, frequency of missed payments, and partial repayments.

Income fluctuations – Variability in earnings that may affect payment capacity.

Behavioral indicators – Communication response rates, engagement with previous payment reminders, and account activity.

By leveraging predictive analytics, businesses can create scoring models that rank customers based on repayment probability. This insight allows collection teams to prioritize at-risk accounts and implement proactive measures before a debt becomes unmanageable.

Rifa’s real-time predictive models analyze multiple data points to determine which customers are at risk of missing payments. These insights enable businesses to send tailored payment plans before the situation escalates, increasing the chances of successful debt recovery.

3. Optimizing Communication Strategies with Data Insights

A generic approach—sending the same reminders to all customers—often results in low engagement and poor recovery rates. Instead, data insights can help optimize communication by tailoring outreach based on individual preferences and behavioral patterns.

Key Considerations for Data-Backed Communication:

Preferred Contact Channels: Data may reveal that some customers respond best to SMS reminders, while others prefer email or phone calls.

Timing Optimization: Analyzing past interactions can indicate the best times to send reminders, such as after work hours or just before due dates.

Personalized Messaging: Customers who have engaged with previous reminders may require a different approach compared to those who have ignored multiple attempts.

4. Automation for Faster and More Efficient Collections

Manually handling debt collection can be time-consuming and inefficient, especially for businesses managing a large volume of accounts. Automation helps streamline key aspects of the process, reducing workload while improving accuracy and speed.

Key Benefits of Automation in Debt Recovery:

Automated Payment Reminders: Scheduled SMS, email, or voice messages ensure customers receive timely notifications without manual follow-ups.

Self-Service Payment Portals: Providing digital payment options allows customers to make payments conveniently, improving collection rates.

Error-Free Data Processing: Automation ensures accurate tracking of due dates, pending amounts, and payment confirmations, eliminating the risk of human errors.

Scalability: Whether handling a hundred or a hundred thousand accounts, automation enables businesses to scale operations without adding extra staff.

5. Real-Time Data Monitoring for Smarter Decision-Making

Static data is not enough for an effective debt collection strategy. Businesses need real-time insights to stay updated on customer behavior and financial status.

How Real-Time Data Helps:

Dynamic Risk Assessment: If a customer’s credit score suddenly drops or their financial activity changes, the system can trigger alerts for immediate follow-up.

Live Payment Tracking: Knowing which customers have partially paid or missed their deadlines helps businesses adjust collection tactics in real-time.

Behavioral Adaptation: If a customer frequently requests deadline extensions, real-time data can identify patterns and recommend tailored repayment plans.

Rifa’s real-time monitoring system provides businesses with up-to-date customer data, allowing them to respond quickly to changing financial conditions. This ensures that debt collection teams can take timely action, improving the overall efficiency of recovery efforts.

Read more: Understanding Benefits and Examples of Automation in Business

Data-Driven Debt Collection

A well-planned debt recovery process isn’t just about chasing overdue payments. By using data effectively, you can improve collection rates, minimize costs, and maintain positive customer relationships. Here’s how data-driven strategies help optimize your debt collection efforts.

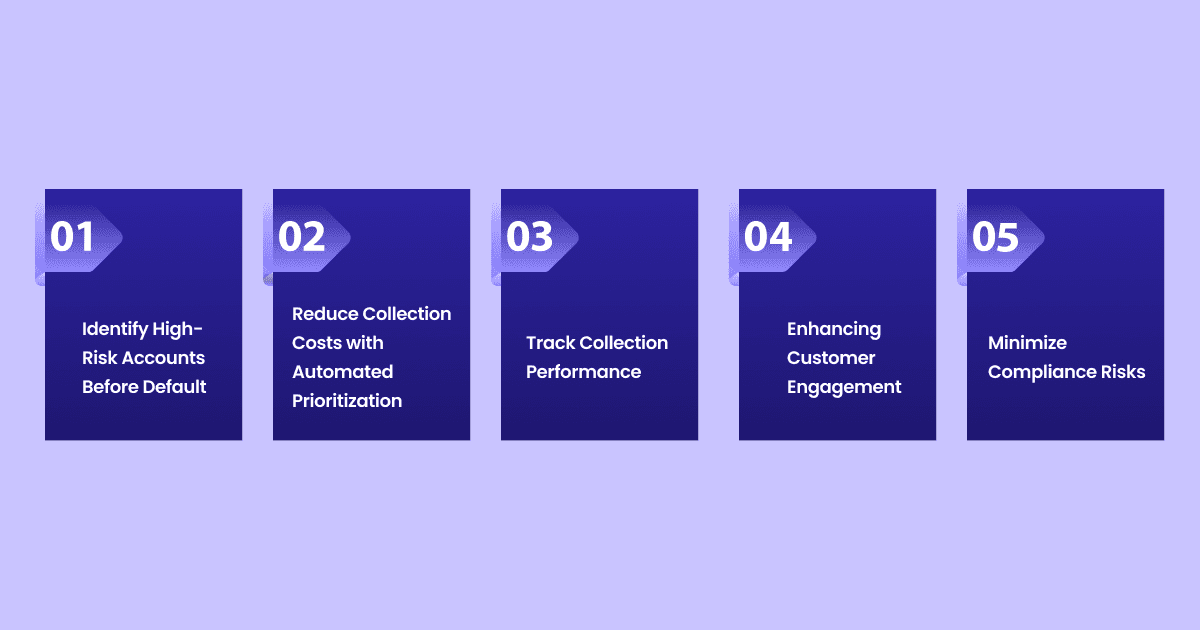

Identify High-Risk Accounts Before Default

Not all overdue accounts require the same approach. Some customers may need a simple reminder, while others pose a high risk of default. Data analysis helps you identify high-risk accounts early, allowing you to intervene before debts become uncollectible.

For example, customers with declining credit scores, repeated late payments, or irregular income patterns are more likely to default. By recognizing these risks early, you can offer tailored solutions—such as payment restructuring or flexible installment plans—before the situation worsens.

Reduce Collection Costs with Automated Prioritization

Manually tracking and reaching out to every overdue account isn’t practical. A data-driven system helps prioritize collections based on recovery likelihood, reducing the time and cost of collection efforts.

For instance, customers who typically pay within a few days of receiving a reminder may not need frequent follow-ups, whereas those with prolonged delays may require direct outreach. Automating this segmentation ensures that your team focuses on high-value cases rather than repetitive tasks.

Rifa AI streamlines this process by automating 70% of routine collection workflows, ensuring that high-risk cases receive immediate attention while minimizing manual workload.

Track Collection Performance

What worked in the past may not be as effective today. Economic conditions, industry trends, and consumer behavior all impact debt collection success. Regular performance tracking helps refine your strategies in real time.

For example, if analysis shows that customers respond better to payment reminders sent in the afternoon rather than the morning, you can adjust your outreach accordingly. If a growing number of customers request payment extensions, it might indicate a need for more flexible repayment plans.

By continuously monitoring and adjusting your approach, you can improve recovery rates while ensuring compliance with evolving financial regulations.

Enhancing Customer Engagement

Debt recovery isn’t just about collection—it’s also about maintaining trust. A generic, aggressive approach can damage relationships and reduce the chances of repayment. Instead, data allows you to personalize communication, improving response rates.

For example, some customers may prefer email reminders, while others respond better to SMS or phone calls. By analyzing past interactions, you can choose the best channel and message tone for each customer. A friendly, informative message explaining payment options is often more effective than a generic demand for payment.

Rifa AI helps personalize debt collection by analyzing response patterns and recommending the best communication channels and timing, ensuring higher engagement and better recovery rates.

Minimize Compliance Risks

Debt collection is subject to strict regulations, and non-compliance can lead to legal issues or reputational damage. Data-driven monitoring ensures that all collection activities align with regulatory standards and customer rights.

For instance, tracking the frequency and tone of communications prevents excessive contact that could be classified as harassment. Automated systems can also flag accounts that require special handling, such as those involving disputes or financial hardship.

By integrating compliance tracking into your debt collection strategy, you can reduce legal risks while maintaining ethical collection practices.

Challenges and Solutions in Data-Driven Debt Recovery

Using data-driven insights can improve debt recovery rates, but it comes with challenges. You need to manage large data volumes, overcome internal resistance, ensure compliance with regulations, and use insights effectively. Here’s how to handle these challenges while optimizing your collection process.

1. Managing Large and Complex Data Sets

You deal with data from multiple sources—customer demographics, payment history, communication logs, and financial trends. Without proper management, this data can become overwhelming, leading to inaccurate analysis and poor decision-making.

Solution: Implement automated data processing tools to organize, filter, and analyze large data sets efficiently. AI-driven platforms help process high-volume data, identify trends, and highlight accounts that need urgent attention. With structured data management, you can make informed decisions faster and improve collection outcomes.

2. Overcoming Resistance to Data-Driven Approaches

If your team is used to traditional collection methods, shifting to a data-driven strategy may meet resistance. Employees might be skeptical of new technologies or fear automation could replace their roles.

Solution: Introduce a data-driven culture by offering training sessions and demonstrating how AI supports—not replaces—human decision-making. Show how automation can handle routine tasks like payment reminders while allowing your team to focus on complex negotiations and customer service. When employees see the benefits firsthand, they’re more likely to adopt data-driven methods.

3. Ensuring Compliance with Data Protection Laws

Debt collection involves handling sensitive customer information, making compliance a major concern. Laws like GDPR and CCPA require strict data security, limiting how you collect, store, and use personal data. Failing to comply can lead to legal penalties and reputational damage.

Solution: Use secure data management systems that include encryption, real-time monitoring, and automated audit trails. Ensuring that all communication follows legal guidelines helps you stay compliant while maintaining customer trust. AI-powered tools can track regulatory changes and adjust collection processes accordingly.

4. Turning Insights into Actionable Strategies

Collecting data isn’t enough—you need to translate insights into effective collection strategies. Many organizations struggle with using predictive analytics effectively, leading to missed recovery opportunities.

Solution: Use AI to analyze debtor behavior and segment accounts based on risk levels. This allows you to prioritize high-risk accounts, personalize communication strategies, and identify the best repayment options. Real-time insights also help you adapt collection tactics based on changing customer behavior.

How Rifa Helps Overcome These Challenges

Rifa AI automates data processing, helping you manage complex datasets without manual effort. It provides real-time risk assessments, ensuring your team focuses on high-priority cases. With built-in compliance tracking, Rifa helps you stay aligned with privacy regulations while improving customer engagement through personalized collection strategies.

Conclusion

Debt collection has changed as a result of data-driven insights for better debt recovery, becoming more successful and efficient. By examining consumer data, you can spot trends and forecast payment patterns, which will help you adjust your collection tactics.

By providing individualized solutions, this strategy not only increases recovery rates but also strengthens client relationships. Adopting and incorporating data-driven tactics is crucial for achieving the best debt collection outcomes.

With technology and data analytics, you can increase your financial results and streamline procedures. Using data to increase efficiency and effectiveness is key to the future of debt collection.

Debt collection is becoming more complex, with rising delinquencies and evolving consumer behaviors. Traditional collection methods often rely on outdated assumptions, leading to inefficiencies, missed opportunities, and strained customer relationships.

The solution? Data-driven insights for better debt recovery. By using customer data—such as payment history, demographics, and behavioral patterns—you can identify high-risk accounts early, tailor collection strategies, and improve recovery rates.

The need for smarter debt collection is growing rapidly. The market for AI-driven debt recovery solutions is projected to surge from USD 3.34 billion in 2024 to USD 15.9 billion by 2034, reflecting a CAGR of 16.90%. This growth underscores the increasing reliance on data analytics, AI, and automation to optimize collections.

In this guide, we’ll break down how to implement data-driven strategies for debt collection, ensuring higher recovery rates, better decision-making, and smarter resource allocation. Let’s dive in.

What Are Data-Driven Insights for Debt Collection?

Debt collection has long been a challenge, with traditional methods often leading to poor recovery rates, high operational costs, and frustrated customers. If you’re relying on generic collection strategies, you might struggle with low response rates, ineffective communication, and wasted resources. That’s where data-driven insights change the game.

Data-driven insights help you move from a reactive to a strategic approach by using real-time data to understand debtor behavior, predict repayment likelihood, and tailor collection efforts. Instead of sending the same reminders to every debtor, you can use intelligent, personalized strategies that improve engagement and increase recovery rates.

Importance of Data-Driven Insights in Debt Collection

A data-driven approach allows businesses to make informed decisions, optimize resources, and improve recovery rates. By utilising data analytics, you can predict payment behaviors, segment customers effectively, and refine communication strategies. Below are the core importance that enhance the efficiency of debt collection efforts.

1. Risk-Based Customer Segmentation

Not all customers who miss payments are the same. Some face temporary financial challenges, while others have a history of defaults. To ensure effective debt collection, businesses need to segment customers based on risk levels using historical data, credit scores, and repayment patterns.

How It Helps:

Prioritization of Collection Efforts: High-risk customers with frequent missed payments or declining credit scores require proactive intervention through personalized repayment plans.

Customized Payment Plans: Medium-risk customers may benefit from flexible settlement options, reducing the likelihood of complete default.

Lower Operational Costs: By allocating resources efficiently, collection teams avoid wasting time on low-risk customers who typically resolve their debts with minimal reminders.

Rifa’s advanced analytics automatically segment customers based on real-time data, identifying high-risk accounts early. This allows businesses to apply targeted strategies, reducing the chances of default while improving recovery rates.

2. Predictive Analytics for Payment Behavior

Predictive analytics enables businesses to anticipate which accounts are likely to default and which customers may need early intervention. This involves analyzing key factors such as:

Payment history – Late payments, frequency of missed payments, and partial repayments.

Income fluctuations – Variability in earnings that may affect payment capacity.

Behavioral indicators – Communication response rates, engagement with previous payment reminders, and account activity.

By leveraging predictive analytics, businesses can create scoring models that rank customers based on repayment probability. This insight allows collection teams to prioritize at-risk accounts and implement proactive measures before a debt becomes unmanageable.

Rifa’s real-time predictive models analyze multiple data points to determine which customers are at risk of missing payments. These insights enable businesses to send tailored payment plans before the situation escalates, increasing the chances of successful debt recovery.

3. Optimizing Communication Strategies with Data Insights

A generic approach—sending the same reminders to all customers—often results in low engagement and poor recovery rates. Instead, data insights can help optimize communication by tailoring outreach based on individual preferences and behavioral patterns.

Key Considerations for Data-Backed Communication:

Preferred Contact Channels: Data may reveal that some customers respond best to SMS reminders, while others prefer email or phone calls.

Timing Optimization: Analyzing past interactions can indicate the best times to send reminders, such as after work hours or just before due dates.

Personalized Messaging: Customers who have engaged with previous reminders may require a different approach compared to those who have ignored multiple attempts.

4. Automation for Faster and More Efficient Collections

Manually handling debt collection can be time-consuming and inefficient, especially for businesses managing a large volume of accounts. Automation helps streamline key aspects of the process, reducing workload while improving accuracy and speed.

Key Benefits of Automation in Debt Recovery:

Automated Payment Reminders: Scheduled SMS, email, or voice messages ensure customers receive timely notifications without manual follow-ups.

Self-Service Payment Portals: Providing digital payment options allows customers to make payments conveniently, improving collection rates.

Error-Free Data Processing: Automation ensures accurate tracking of due dates, pending amounts, and payment confirmations, eliminating the risk of human errors.

Scalability: Whether handling a hundred or a hundred thousand accounts, automation enables businesses to scale operations without adding extra staff.

5. Real-Time Data Monitoring for Smarter Decision-Making

Static data is not enough for an effective debt collection strategy. Businesses need real-time insights to stay updated on customer behavior and financial status.

How Real-Time Data Helps:

Dynamic Risk Assessment: If a customer’s credit score suddenly drops or their financial activity changes, the system can trigger alerts for immediate follow-up.

Live Payment Tracking: Knowing which customers have partially paid or missed their deadlines helps businesses adjust collection tactics in real-time.

Behavioral Adaptation: If a customer frequently requests deadline extensions, real-time data can identify patterns and recommend tailored repayment plans.

Rifa’s real-time monitoring system provides businesses with up-to-date customer data, allowing them to respond quickly to changing financial conditions. This ensures that debt collection teams can take timely action, improving the overall efficiency of recovery efforts.

Read more: Understanding Benefits and Examples of Automation in Business

Data-Driven Debt Collection

A well-planned debt recovery process isn’t just about chasing overdue payments. By using data effectively, you can improve collection rates, minimize costs, and maintain positive customer relationships. Here’s how data-driven strategies help optimize your debt collection efforts.

Identify High-Risk Accounts Before Default

Not all overdue accounts require the same approach. Some customers may need a simple reminder, while others pose a high risk of default. Data analysis helps you identify high-risk accounts early, allowing you to intervene before debts become uncollectible.

For example, customers with declining credit scores, repeated late payments, or irregular income patterns are more likely to default. By recognizing these risks early, you can offer tailored solutions—such as payment restructuring or flexible installment plans—before the situation worsens.

Reduce Collection Costs with Automated Prioritization

Manually tracking and reaching out to every overdue account isn’t practical. A data-driven system helps prioritize collections based on recovery likelihood, reducing the time and cost of collection efforts.

For instance, customers who typically pay within a few days of receiving a reminder may not need frequent follow-ups, whereas those with prolonged delays may require direct outreach. Automating this segmentation ensures that your team focuses on high-value cases rather than repetitive tasks.

Rifa AI streamlines this process by automating 70% of routine collection workflows, ensuring that high-risk cases receive immediate attention while minimizing manual workload.

Track Collection Performance

What worked in the past may not be as effective today. Economic conditions, industry trends, and consumer behavior all impact debt collection success. Regular performance tracking helps refine your strategies in real time.

For example, if analysis shows that customers respond better to payment reminders sent in the afternoon rather than the morning, you can adjust your outreach accordingly. If a growing number of customers request payment extensions, it might indicate a need for more flexible repayment plans.

By continuously monitoring and adjusting your approach, you can improve recovery rates while ensuring compliance with evolving financial regulations.

Enhancing Customer Engagement

Debt recovery isn’t just about collection—it’s also about maintaining trust. A generic, aggressive approach can damage relationships and reduce the chances of repayment. Instead, data allows you to personalize communication, improving response rates.

For example, some customers may prefer email reminders, while others respond better to SMS or phone calls. By analyzing past interactions, you can choose the best channel and message tone for each customer. A friendly, informative message explaining payment options is often more effective than a generic demand for payment.

Rifa AI helps personalize debt collection by analyzing response patterns and recommending the best communication channels and timing, ensuring higher engagement and better recovery rates.

Minimize Compliance Risks

Debt collection is subject to strict regulations, and non-compliance can lead to legal issues or reputational damage. Data-driven monitoring ensures that all collection activities align with regulatory standards and customer rights.

For instance, tracking the frequency and tone of communications prevents excessive contact that could be classified as harassment. Automated systems can also flag accounts that require special handling, such as those involving disputes or financial hardship.

By integrating compliance tracking into your debt collection strategy, you can reduce legal risks while maintaining ethical collection practices.

Challenges and Solutions in Data-Driven Debt Recovery

Using data-driven insights can improve debt recovery rates, but it comes with challenges. You need to manage large data volumes, overcome internal resistance, ensure compliance with regulations, and use insights effectively. Here’s how to handle these challenges while optimizing your collection process.

1. Managing Large and Complex Data Sets

You deal with data from multiple sources—customer demographics, payment history, communication logs, and financial trends. Without proper management, this data can become overwhelming, leading to inaccurate analysis and poor decision-making.

Solution: Implement automated data processing tools to organize, filter, and analyze large data sets efficiently. AI-driven platforms help process high-volume data, identify trends, and highlight accounts that need urgent attention. With structured data management, you can make informed decisions faster and improve collection outcomes.

2. Overcoming Resistance to Data-Driven Approaches

If your team is used to traditional collection methods, shifting to a data-driven strategy may meet resistance. Employees might be skeptical of new technologies or fear automation could replace their roles.

Solution: Introduce a data-driven culture by offering training sessions and demonstrating how AI supports—not replaces—human decision-making. Show how automation can handle routine tasks like payment reminders while allowing your team to focus on complex negotiations and customer service. When employees see the benefits firsthand, they’re more likely to adopt data-driven methods.

3. Ensuring Compliance with Data Protection Laws

Debt collection involves handling sensitive customer information, making compliance a major concern. Laws like GDPR and CCPA require strict data security, limiting how you collect, store, and use personal data. Failing to comply can lead to legal penalties and reputational damage.

Solution: Use secure data management systems that include encryption, real-time monitoring, and automated audit trails. Ensuring that all communication follows legal guidelines helps you stay compliant while maintaining customer trust. AI-powered tools can track regulatory changes and adjust collection processes accordingly.

4. Turning Insights into Actionable Strategies

Collecting data isn’t enough—you need to translate insights into effective collection strategies. Many organizations struggle with using predictive analytics effectively, leading to missed recovery opportunities.

Solution: Use AI to analyze debtor behavior and segment accounts based on risk levels. This allows you to prioritize high-risk accounts, personalize communication strategies, and identify the best repayment options. Real-time insights also help you adapt collection tactics based on changing customer behavior.

How Rifa Helps Overcome These Challenges

Rifa AI automates data processing, helping you manage complex datasets without manual effort. It provides real-time risk assessments, ensuring your team focuses on high-priority cases. With built-in compliance tracking, Rifa helps you stay aligned with privacy regulations while improving customer engagement through personalized collection strategies.

Conclusion

Debt collection has changed as a result of data-driven insights for better debt recovery, becoming more successful and efficient. By examining consumer data, you can spot trends and forecast payment patterns, which will help you adjust your collection tactics.

By providing individualized solutions, this strategy not only increases recovery rates but also strengthens client relationships. Adopting and incorporating data-driven tactics is crucial for achieving the best debt collection outcomes.

With technology and data analytics, you can increase your financial results and streamline procedures. Using data to increase efficiency and effectiveness is key to the future of debt collection.

Mar 17, 2025

Mar 17, 2025

Mar 17, 2025

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved