How to Negotiate and Reduce Debt Collection Costs

How to Negotiate and Reduce Debt Collection Costs

How to Negotiate and Reduce Debt Collection Costs

How to Negotiate and Reduce Debt Collection Costs

Anant Sharma

Anant Sharma

Anant Sharma

A bank executive once described debt collection as “trying to fill a leaking bucket.” No matter how much effort goes into chasing payments, inefficiencies and rising costs often undermine the results.

For businesses like banks, credit unions, and insurance companies, debt collection isn’t just about recovering money—it’s about doing so efficiently while maintaining a positive customer experience. From hiring staff for follow-ups to paying third-party agencies, the expenses add up quickly—eating into revenue that should fuel business growth.

Negotiating with customers and agencies is key to successful debt collection. It helps secure timely repayments while maintaining positive relationships. Offering flexible payment plans and understanding the debtor’s situation can improve recovery rates, but managing these negotiations manually can be time-consuming and costly.

Automation offers a smarter way forward. Businesses can streamline their collection process by using AI-driven negotiation, predictive analytics, and automated payment reminders while reducing costs.

In this blog, we will explore how your business can take control of its debt recovery strategy, cut expenses, and improve customer relationships—all with the right mix of negotiation tactics and automation.

What are Debt Collection Costs?

Debt collection costs refer to the expenses incurred by businesses in recovering unpaid debts. These costs can include labor expenses for in-house collection teams, fees paid to third-party collection agencies, legal costs associated with pursuing delinquent accounts, communication expenses (such as phone calls, emails, and postage), and investments in debt collection software or automation tools.

While these expenses are necessary for maintaining cash flow and minimizing bad debt losses, they can quickly add up if not optimized. Businesses must strike a balance between effective debt recovery and cost efficiency by implementing strategic collection practices, using technology, and continuously monitoring their collection performance.

If not managed properly, these expenses can significantly impact a company's bottom line, reducing the overall profitability of lending and credit-based businesses.

Why Do Debt Collection Costs Keep Rising?

Debt collection costs tend to rise over time due to several compounding factors. As debts age, the likelihood of recovery decreases, requiring more aggressive and resource-intensive collection efforts. Businesses may need to engage third-party agencies or legal services, both of which come with high fees that can range from a percentage of the recovered amount to fixed legal expenses.

Compliance regulations demand ongoing investments in staff training, secure data handling, and documentation, adding to operational expenses. Additionally, manual collection efforts—such as repeated follow-ups, payment tracking, and dispute resolution—consume valuable time and resources. If left unmanaged, these rising expenses can significantly reduce the net amount recovered from outstanding debts.

Why should Businesses Negotiate Debt Collection Costs?

Businesses should negotiate debt collection costs to protect their bottom line and maximize recoveries. Without strategic cost control, rising expenses—such as agency fees, legal charges, and administrative overhead—can significantly reduce the actual amount recovered. Additionally, inefficient collection processes can strain cash flow, forcing businesses to allocate more resources to overdue accounts instead of growth initiatives.

Unchecked costs can also lead to excessive reliance on third-party agencies, reducing profit margins and making debt recovery unsustainable in the long run. By negotiating smarter terms and optimizing their collection strategies, businesses can ensure that the cost of recovering debt doesn’t outweigh the value of what’s being recovered.

In the next section, we will explore effective strategies for negotiating and reducing debt collection costs, helping your business recover debts more efficiently while maintaining profitability.

Strategic Negotiation for Reduced Debt Collection Costs

Effective debt collection is essential for maintaining cash flow, but the costs associated with recovering outstanding payments can quickly add up. Businesses must adopt strategic negotiation tactics to reduce these costs while ensuring sustainable debt recovery.

Below, we will explore different negotiation strategies, cost-effective approaches, and how automation can ease your debt collection process.

Internal vs. External Collection Agencies

Debt collection is a critical function for businesses aiming to recover outstanding payments efficiently. Companies must decide whether to manage collections internally or outsource to third-party agencies. This decision involves evaluating costs, operational efficiency, and control over customer relationships.

Internal Debt Collection

Internal debt collection enables businesses to recover outstanding payments while maintaining customer relationships. A structured approach ensures efficiency, compliance, and cost savings without relying on third-party agencies.

Advantages

Full Control – Businesses maintain direct oversight of customer interactions and tailor collection strategies to their needs.

Brand Protection – Internal teams ensure a customer-centric approach, preserving relationships and minimizing reputational risk.

Integration with Existing Processes – Seamless integration with CRM and accounting systems allows for personalized communication and streamlined data tracking.

Disadvantages

High Labor Costs – Maintaining an in-house collection team requires salaries, benefits, and performance incentives.

Training Expenses – Employees must be regularly trained in compliance, negotiation tactics, and customer engagement.

Operational Overhead – Infrastructure costs, including call centers and debt recovery software, add to the total expense.

External Debt Collection Agencies

External debt collection agencies help businesses recover overdue payments by leveraging specialized expertise and resources. They handle escalated cases, ensuring higher recovery rates while allowing companies to focus on core operations.

Advantages

Reduced Operational Burden – Outsourcing relieves businesses from managing collection teams and administrative overhead.

Expertise & Compliance – Agencies have specialized knowledge in debt recovery and adhere to legal regulations.

Higher Success Rates – Professional collectors use established techniques and psychological triggers to maximize recovery rates.

Disadvantages

High Fees – Agencies typically charge 10% to 50% of recovered amounts, significantly impacting profitability.

Loss of Customer Relationships – Third-party interactions can be less personalized, potentially damaging customer goodwill.

Limited Control – Businesses may have less influence over communication strategies and recovery approaches.

Negotiation Strategies for Lowering External Collection Costs

To mitigate the high costs associated with outsourcing collections, businesses can adopt the following negotiation strategies:

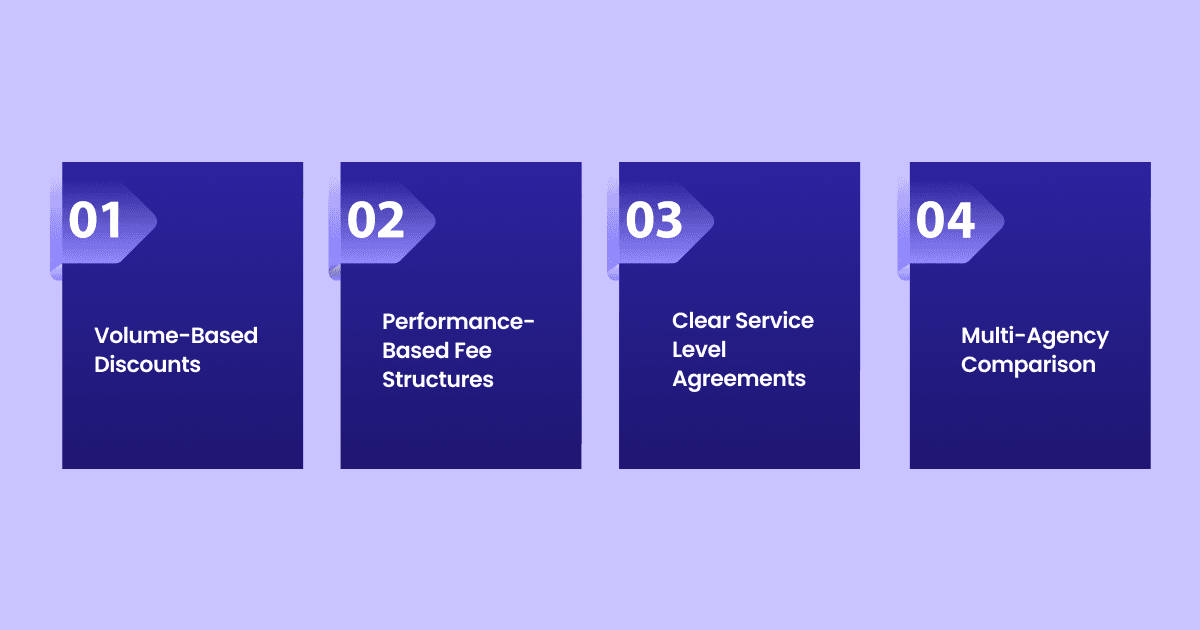

Volume-Based Discounts

Businesses that send a high volume of delinquent accounts to collection agencies can leverage economies of scale to negotiate lower fees.

Agencies often offer tiered pricing models where the cost per account decreases as the volume increases. For example, a collection agency might charge 30% of the recovered amount for up to 100 accounts but lower the fee to 20% for businesses submitting over 500 accounts, making bulk submissions more cost-effective.

Companies should analyze their historical debt recovery trends and use data-driven projections to negotiate bulk discounts.

Performance-Based Fee Structures

Rather than agreeing to a flat percentage on all recovered amounts, businesses can push for a fee model based on actual collection performance. This structure aligns the agency’s incentives with the company’s financial goals.

For example, agencies could receive a higher percentage for collecting older or high-risk debts while charging a lower rate for easier-to-recover accounts.

Businesses should request historical performance data from agencies and establish success benchmarks before finalizing contracts.

Clear Service Level Agreements (SLAs)

Establishing detailed SLAs ensures that agencies meet specific efficiency, compliance, and responsiveness standards.

These agreements should define key performance metrics such as recovery rates, response times, dispute resolution effectiveness, and adherence to regulatory guidelines.

Regular performance reviews and penalty clauses for non-compliance help maintain accountability and ensure that the business receives high-quality service.

Multi-Agency Comparison

Conducting a thorough comparison of multiple collection agencies allows businesses to identify the most cost-effective and efficient partner. This process should include evaluating each agency’s fee structure, historical recovery rates, industry expertise, and customer service approach.

Companies can request detailed proposals and negotiate with multiple agencies to secure the best terms.

Additionally, adopting a hybrid approach—using different agencies for different types of debts—can optimize recovery efforts and minimize overall costs.

Rifa AI specializes in automating early-stage debt collection, reducing reliance on costly third-party agencies. Its AI-powered voice bots and predictive analytics optimize debtor engagement, ensuring higher recovery rates at lower costs.

By streamlining follow-ups and negotiations, Rifa AI minimizes outsourcing needs while maintaining compliance and customer relationships.

Early Payment Incentives: Encouraging Timely Repayments

Encouraging customers to settle their dues ahead of time can significantly reduce delinquent accounts, enhance liquidity, and improve overall financial stability. By offering tangible incentives and leveraging AI-driven automation, businesses can create a system that prioritizes early payments while maintaining debtor engagement.

Discounts for Early Payments: Implement structured discount tiers (e.g., 2% for payments within 10 days, 5% within 5 days) to encourage early settlements. Businesses using dynamic discounting models have seen up to a 25% reduction in late payments and stronger cash flow consistency.

Loyalty Perks for Timely Payers: Offering benefits such as extended credit limits, waived late fees, or exclusive discounts fosters a culture of reliability and prompt payments, leading to long-term debtor engagement.

Gamification & Rewards: Integrate a point-based rewards system where debtors earn points for early payments, redeemable for discounts, service upgrades, or financial incentives.

Rifa AI enhances early payment adoption by automating personalized payment reminders, dynamically adjusting incentive structures, and utilizing AI-powered voice interactions. With a 40% higher payment conversion rate and 30% faster debt recovery, businesses experience improved liquidity and reduced delinquencies.

Strategic Payment Structuring: Flexible and Effective Plans

When full payments aren’t feasible, businesses can improve debt recovery by offering structured repayment options that accommodate debtor financial conditions. By leveraging AI and predictive analytics, organizations can create personalized plans that minimize defaults while maintaining debtor trust.

Tiered Payment Plans

Gradual repayment structures help debtors ease into financial commitments without overwhelming their cash flow. Initial payments start small and gradually increase, giving debtors time to adjust while maintaining consistency in repayments.

Milestone-Based Settlements

Aligning payment deadlines with key financial inflows—such as payroll cycles, seasonal revenue spikes, or business cash flow patterns—ensures debtors can meet obligations without excessive financial stress. This approach enhances affordability and improves compliance rates.

Interest-Free Short-Term Settlements

Offering zero-interest repayment options for shorter terms incentivizes debtors to settle dues faster. This strategy not only speeds up collections but also strengthens debtor relationships, increasing the likelihood of future financial cooperation.

Automated Payment Tracking & Compliance

AI-powered systems monitor upcoming and missed payments in real time, triggering proactive reminders and follow-ups. These systems help businesses maintain compliance, reduce delinquency rates, and optimize collection workflows by ensuring debtors stay on track.

Rifa AI's intelligent Voice Agents negotiate customized repayment terms based on debtor data, dynamically adjust payment schedules, and ensure compliance through AI-driven decision trees. By integrating seamlessly with CRM and ERP systems, collection efficiency doubles, and delinquency rates decrease significantly.

Multi-Channel Engagement: Expanding Debtor Reach

A single-channel debt collection approach often fails to engage all debtors effectively. By leveraging an omnichannel strategy powered by AI, businesses can maximize outreach, improve debtor response rates, and enhance recovery efforts.

Omnichannel Contact Strategies

AI-driven automation ensures synchronized communication across multiple platforms, including voice calls, SMS, email, WhatsApp, and in-app notifications.

This multi-touchpoint approach increases debtor accessibility, allowing them to interact through their preferred channel and improving engagement rates.

Interactive Self-Service Portals

AI-powered portals give debtors full control over their accounts. They can check outstanding balances, explore customized repayment options, and make payments independently, reducing the need for agent intervention.

These portals enhance convenience and encourage faster resolutions.

Automated Follow-Up Sequences

Intelligent scheduling systems analyze debtor behavior and dynamically adjust follow-up intensity. If a debtor shows signs of willingness to pay, the system may reduce outreach frequency.

If a debtor is unresponsive, the AI escalates reminders strategically, ensuring effective communication without overwhelming debtors or collectors.

AI-Powered Chatbots for 24/7 Assistance

Virtual assistants handle debtor inquiries around the clock, providing instant responses on payment options, settlement plans, and due dates.

Chatbots also schedule callbacks when human intervention is necessary, streamlining support while ensuring continuous debtor engagement.

Rifa AI continuously analyzes debtor behavior, refines call strategies dynamically, and personalizes communication to maximize engagement. With over 2 million calls automated and a 3x increase in collection success, Rifa AI ensures debt recovery remains efficient, empathetic, and compliant.

Legal & Compliance-Based Leverage: Risk-Free Collections

Balancing compliance with strategic debt recovery measures is crucial to maintaining ethical standards while maximizing collections. AI-driven compliance monitoring ensures businesses adhere to legal frameworks, reducing regulatory risks and enhancing credibility.

Soft Legal Warnings

Carefully crafted, compliance-focused notices inform debtors of potential legal consequences without resorting to aggressive tactics. These communications create a sense of urgency while preserving debtor relationships and mitigating reputational risks.

Pre-Litigation Settlements

Before initiating legal action, businesses can offer structured settlement options that allow debtors to resolve outstanding balances amicably. This approach helps avoid costly litigation while accelerating recoveries.

Regulatory Compliance Assurance

Strict adherence to industry regulations such as the Fair Debt Collection Practices Act (FDCPA), Health Insurance Portability and Accountability Act (HIPAA), and SOC 2 standards ensures lawful debt recovery practices. Compliance protects businesses from lawsuits, fines, and reputational damage.

Automated Compliance Monitoring

AI-powered tools track collection activities in real-time, flagging potential compliance violations and maintaining audit-ready documentation. This proactive approach minimizes legal risks and ensures adherence to industry standards.

Rifa AI automates legally compliant call scripts, monitors interactions for regulatory adherence, and maintains audit-ready records. With full compliance with FDCPA, HIPAA, and SOC 2 Type 1 & 2, businesses can recover debts ethically while minimizing legal exposure.

Alternative Collection Models: Innovative Approaches

Traditional debt collection methods often rely on external agencies, leading to high costs and limited control. By adopting AI-driven alternative collection models, businesses can optimize recoveries while reducing dependency on third-party collectors.

Revenue Sharing Agreements

Instead of paying fixed fees to collection agencies, businesses can establish performance-based commission structures with partners.

This aligns incentives, ensuring that recovery efforts remain efficient and cost-effective.

Debt Buyback Programs

Organizations can repurchase written-off debts under negotiated terms, allowing them to recover a portion of lost revenue.

AI-powered insights help identify high-potential accounts, optimizing long-term financial outcomes.

AI-Driven Third-Party Negotiation

AI-powered mediators act as neutral facilitators in debt settlements, increasing debtor cooperation while minimizing disputes.

These automated systems adapt negotiation strategies based on debtor responses, improving settlement rates.

Predictive Collection Models

Machine learning analyzes debtor profiles, payment history, and behavioral patterns to determine the most effective recovery strategy.

By predicting the likelihood of repayment, businesses can focus resources where they yield the highest returns.

Rifa AI streamlines third-party negotiations, optimizes revenue-sharing agreements, and enhances recovery through AI-driven mediation. With predictive analytics, collection costs reduce by over 50%, ensuring businesses recover debts efficiently and ethically.

Collect Faster and Spend Less with Rifa AI

As regulations tighten and customer expectations evolve, businesses need an agile, compliant, and scalable debt collection strategy. The right technology can balance business efficiency with customer fairness, ensuring compliance and long-term trust.

Debt collection requires a careful balance of efficiency, compliance, and customer experience—Rifa AI delivers on all three. Rifa AI provides a scalable, AI-driven collection solution that evolves with business needs. From startups to enterprises, our automated outreach, intelligent risk analysis, and self-service portals ensure consistent, cost-effective recovery.

Rifa AI automates 10,000+ calls daily, delivering personalized payment reminders, automated dispute resolution, and seamless CRM updates. Our AI ensures 15%+ right-party contact rates, 5.2-minute call handling times, and zero compliance issues, outperforming industry standards.

Schedule a demo today and see how Rifa AI can cut collection costs by 50%+ while boosting recovery rates.

A bank executive once described debt collection as “trying to fill a leaking bucket.” No matter how much effort goes into chasing payments, inefficiencies and rising costs often undermine the results.

For businesses like banks, credit unions, and insurance companies, debt collection isn’t just about recovering money—it’s about doing so efficiently while maintaining a positive customer experience. From hiring staff for follow-ups to paying third-party agencies, the expenses add up quickly—eating into revenue that should fuel business growth.

Negotiating with customers and agencies is key to successful debt collection. It helps secure timely repayments while maintaining positive relationships. Offering flexible payment plans and understanding the debtor’s situation can improve recovery rates, but managing these negotiations manually can be time-consuming and costly.

Automation offers a smarter way forward. Businesses can streamline their collection process by using AI-driven negotiation, predictive analytics, and automated payment reminders while reducing costs.

In this blog, we will explore how your business can take control of its debt recovery strategy, cut expenses, and improve customer relationships—all with the right mix of negotiation tactics and automation.

What are Debt Collection Costs?

Debt collection costs refer to the expenses incurred by businesses in recovering unpaid debts. These costs can include labor expenses for in-house collection teams, fees paid to third-party collection agencies, legal costs associated with pursuing delinquent accounts, communication expenses (such as phone calls, emails, and postage), and investments in debt collection software or automation tools.

While these expenses are necessary for maintaining cash flow and minimizing bad debt losses, they can quickly add up if not optimized. Businesses must strike a balance between effective debt recovery and cost efficiency by implementing strategic collection practices, using technology, and continuously monitoring their collection performance.

If not managed properly, these expenses can significantly impact a company's bottom line, reducing the overall profitability of lending and credit-based businesses.

Why Do Debt Collection Costs Keep Rising?

Debt collection costs tend to rise over time due to several compounding factors. As debts age, the likelihood of recovery decreases, requiring more aggressive and resource-intensive collection efforts. Businesses may need to engage third-party agencies or legal services, both of which come with high fees that can range from a percentage of the recovered amount to fixed legal expenses.

Compliance regulations demand ongoing investments in staff training, secure data handling, and documentation, adding to operational expenses. Additionally, manual collection efforts—such as repeated follow-ups, payment tracking, and dispute resolution—consume valuable time and resources. If left unmanaged, these rising expenses can significantly reduce the net amount recovered from outstanding debts.

Why should Businesses Negotiate Debt Collection Costs?

Businesses should negotiate debt collection costs to protect their bottom line and maximize recoveries. Without strategic cost control, rising expenses—such as agency fees, legal charges, and administrative overhead—can significantly reduce the actual amount recovered. Additionally, inefficient collection processes can strain cash flow, forcing businesses to allocate more resources to overdue accounts instead of growth initiatives.

Unchecked costs can also lead to excessive reliance on third-party agencies, reducing profit margins and making debt recovery unsustainable in the long run. By negotiating smarter terms and optimizing their collection strategies, businesses can ensure that the cost of recovering debt doesn’t outweigh the value of what’s being recovered.

In the next section, we will explore effective strategies for negotiating and reducing debt collection costs, helping your business recover debts more efficiently while maintaining profitability.

Strategic Negotiation for Reduced Debt Collection Costs

Effective debt collection is essential for maintaining cash flow, but the costs associated with recovering outstanding payments can quickly add up. Businesses must adopt strategic negotiation tactics to reduce these costs while ensuring sustainable debt recovery.

Below, we will explore different negotiation strategies, cost-effective approaches, and how automation can ease your debt collection process.

Internal vs. External Collection Agencies

Debt collection is a critical function for businesses aiming to recover outstanding payments efficiently. Companies must decide whether to manage collections internally or outsource to third-party agencies. This decision involves evaluating costs, operational efficiency, and control over customer relationships.

Internal Debt Collection

Internal debt collection enables businesses to recover outstanding payments while maintaining customer relationships. A structured approach ensures efficiency, compliance, and cost savings without relying on third-party agencies.

Advantages

Full Control – Businesses maintain direct oversight of customer interactions and tailor collection strategies to their needs.

Brand Protection – Internal teams ensure a customer-centric approach, preserving relationships and minimizing reputational risk.

Integration with Existing Processes – Seamless integration with CRM and accounting systems allows for personalized communication and streamlined data tracking.

Disadvantages

High Labor Costs – Maintaining an in-house collection team requires salaries, benefits, and performance incentives.

Training Expenses – Employees must be regularly trained in compliance, negotiation tactics, and customer engagement.

Operational Overhead – Infrastructure costs, including call centers and debt recovery software, add to the total expense.

External Debt Collection Agencies

External debt collection agencies help businesses recover overdue payments by leveraging specialized expertise and resources. They handle escalated cases, ensuring higher recovery rates while allowing companies to focus on core operations.

Advantages

Reduced Operational Burden – Outsourcing relieves businesses from managing collection teams and administrative overhead.

Expertise & Compliance – Agencies have specialized knowledge in debt recovery and adhere to legal regulations.

Higher Success Rates – Professional collectors use established techniques and psychological triggers to maximize recovery rates.

Disadvantages

High Fees – Agencies typically charge 10% to 50% of recovered amounts, significantly impacting profitability.

Loss of Customer Relationships – Third-party interactions can be less personalized, potentially damaging customer goodwill.

Limited Control – Businesses may have less influence over communication strategies and recovery approaches.

Negotiation Strategies for Lowering External Collection Costs

To mitigate the high costs associated with outsourcing collections, businesses can adopt the following negotiation strategies:

Volume-Based Discounts

Businesses that send a high volume of delinquent accounts to collection agencies can leverage economies of scale to negotiate lower fees.

Agencies often offer tiered pricing models where the cost per account decreases as the volume increases. For example, a collection agency might charge 30% of the recovered amount for up to 100 accounts but lower the fee to 20% for businesses submitting over 500 accounts, making bulk submissions more cost-effective.

Companies should analyze their historical debt recovery trends and use data-driven projections to negotiate bulk discounts.

Performance-Based Fee Structures

Rather than agreeing to a flat percentage on all recovered amounts, businesses can push for a fee model based on actual collection performance. This structure aligns the agency’s incentives with the company’s financial goals.

For example, agencies could receive a higher percentage for collecting older or high-risk debts while charging a lower rate for easier-to-recover accounts.

Businesses should request historical performance data from agencies and establish success benchmarks before finalizing contracts.

Clear Service Level Agreements (SLAs)

Establishing detailed SLAs ensures that agencies meet specific efficiency, compliance, and responsiveness standards.

These agreements should define key performance metrics such as recovery rates, response times, dispute resolution effectiveness, and adherence to regulatory guidelines.

Regular performance reviews and penalty clauses for non-compliance help maintain accountability and ensure that the business receives high-quality service.

Multi-Agency Comparison

Conducting a thorough comparison of multiple collection agencies allows businesses to identify the most cost-effective and efficient partner. This process should include evaluating each agency’s fee structure, historical recovery rates, industry expertise, and customer service approach.

Companies can request detailed proposals and negotiate with multiple agencies to secure the best terms.

Additionally, adopting a hybrid approach—using different agencies for different types of debts—can optimize recovery efforts and minimize overall costs.

Rifa AI specializes in automating early-stage debt collection, reducing reliance on costly third-party agencies. Its AI-powered voice bots and predictive analytics optimize debtor engagement, ensuring higher recovery rates at lower costs.

By streamlining follow-ups and negotiations, Rifa AI minimizes outsourcing needs while maintaining compliance and customer relationships.

Early Payment Incentives: Encouraging Timely Repayments

Encouraging customers to settle their dues ahead of time can significantly reduce delinquent accounts, enhance liquidity, and improve overall financial stability. By offering tangible incentives and leveraging AI-driven automation, businesses can create a system that prioritizes early payments while maintaining debtor engagement.

Discounts for Early Payments: Implement structured discount tiers (e.g., 2% for payments within 10 days, 5% within 5 days) to encourage early settlements. Businesses using dynamic discounting models have seen up to a 25% reduction in late payments and stronger cash flow consistency.

Loyalty Perks for Timely Payers: Offering benefits such as extended credit limits, waived late fees, or exclusive discounts fosters a culture of reliability and prompt payments, leading to long-term debtor engagement.

Gamification & Rewards: Integrate a point-based rewards system where debtors earn points for early payments, redeemable for discounts, service upgrades, or financial incentives.

Rifa AI enhances early payment adoption by automating personalized payment reminders, dynamically adjusting incentive structures, and utilizing AI-powered voice interactions. With a 40% higher payment conversion rate and 30% faster debt recovery, businesses experience improved liquidity and reduced delinquencies.

Strategic Payment Structuring: Flexible and Effective Plans

When full payments aren’t feasible, businesses can improve debt recovery by offering structured repayment options that accommodate debtor financial conditions. By leveraging AI and predictive analytics, organizations can create personalized plans that minimize defaults while maintaining debtor trust.

Tiered Payment Plans

Gradual repayment structures help debtors ease into financial commitments without overwhelming their cash flow. Initial payments start small and gradually increase, giving debtors time to adjust while maintaining consistency in repayments.

Milestone-Based Settlements

Aligning payment deadlines with key financial inflows—such as payroll cycles, seasonal revenue spikes, or business cash flow patterns—ensures debtors can meet obligations without excessive financial stress. This approach enhances affordability and improves compliance rates.

Interest-Free Short-Term Settlements

Offering zero-interest repayment options for shorter terms incentivizes debtors to settle dues faster. This strategy not only speeds up collections but also strengthens debtor relationships, increasing the likelihood of future financial cooperation.

Automated Payment Tracking & Compliance

AI-powered systems monitor upcoming and missed payments in real time, triggering proactive reminders and follow-ups. These systems help businesses maintain compliance, reduce delinquency rates, and optimize collection workflows by ensuring debtors stay on track.

Rifa AI's intelligent Voice Agents negotiate customized repayment terms based on debtor data, dynamically adjust payment schedules, and ensure compliance through AI-driven decision trees. By integrating seamlessly with CRM and ERP systems, collection efficiency doubles, and delinquency rates decrease significantly.

Multi-Channel Engagement: Expanding Debtor Reach

A single-channel debt collection approach often fails to engage all debtors effectively. By leveraging an omnichannel strategy powered by AI, businesses can maximize outreach, improve debtor response rates, and enhance recovery efforts.

Omnichannel Contact Strategies

AI-driven automation ensures synchronized communication across multiple platforms, including voice calls, SMS, email, WhatsApp, and in-app notifications.

This multi-touchpoint approach increases debtor accessibility, allowing them to interact through their preferred channel and improving engagement rates.

Interactive Self-Service Portals

AI-powered portals give debtors full control over their accounts. They can check outstanding balances, explore customized repayment options, and make payments independently, reducing the need for agent intervention.

These portals enhance convenience and encourage faster resolutions.

Automated Follow-Up Sequences

Intelligent scheduling systems analyze debtor behavior and dynamically adjust follow-up intensity. If a debtor shows signs of willingness to pay, the system may reduce outreach frequency.

If a debtor is unresponsive, the AI escalates reminders strategically, ensuring effective communication without overwhelming debtors or collectors.

AI-Powered Chatbots for 24/7 Assistance

Virtual assistants handle debtor inquiries around the clock, providing instant responses on payment options, settlement plans, and due dates.

Chatbots also schedule callbacks when human intervention is necessary, streamlining support while ensuring continuous debtor engagement.

Rifa AI continuously analyzes debtor behavior, refines call strategies dynamically, and personalizes communication to maximize engagement. With over 2 million calls automated and a 3x increase in collection success, Rifa AI ensures debt recovery remains efficient, empathetic, and compliant.

Legal & Compliance-Based Leverage: Risk-Free Collections

Balancing compliance with strategic debt recovery measures is crucial to maintaining ethical standards while maximizing collections. AI-driven compliance monitoring ensures businesses adhere to legal frameworks, reducing regulatory risks and enhancing credibility.

Soft Legal Warnings

Carefully crafted, compliance-focused notices inform debtors of potential legal consequences without resorting to aggressive tactics. These communications create a sense of urgency while preserving debtor relationships and mitigating reputational risks.

Pre-Litigation Settlements

Before initiating legal action, businesses can offer structured settlement options that allow debtors to resolve outstanding balances amicably. This approach helps avoid costly litigation while accelerating recoveries.

Regulatory Compliance Assurance

Strict adherence to industry regulations such as the Fair Debt Collection Practices Act (FDCPA), Health Insurance Portability and Accountability Act (HIPAA), and SOC 2 standards ensures lawful debt recovery practices. Compliance protects businesses from lawsuits, fines, and reputational damage.

Automated Compliance Monitoring

AI-powered tools track collection activities in real-time, flagging potential compliance violations and maintaining audit-ready documentation. This proactive approach minimizes legal risks and ensures adherence to industry standards.

Rifa AI automates legally compliant call scripts, monitors interactions for regulatory adherence, and maintains audit-ready records. With full compliance with FDCPA, HIPAA, and SOC 2 Type 1 & 2, businesses can recover debts ethically while minimizing legal exposure.

Alternative Collection Models: Innovative Approaches

Traditional debt collection methods often rely on external agencies, leading to high costs and limited control. By adopting AI-driven alternative collection models, businesses can optimize recoveries while reducing dependency on third-party collectors.

Revenue Sharing Agreements

Instead of paying fixed fees to collection agencies, businesses can establish performance-based commission structures with partners.

This aligns incentives, ensuring that recovery efforts remain efficient and cost-effective.

Debt Buyback Programs

Organizations can repurchase written-off debts under negotiated terms, allowing them to recover a portion of lost revenue.

AI-powered insights help identify high-potential accounts, optimizing long-term financial outcomes.

AI-Driven Third-Party Negotiation

AI-powered mediators act as neutral facilitators in debt settlements, increasing debtor cooperation while minimizing disputes.

These automated systems adapt negotiation strategies based on debtor responses, improving settlement rates.

Predictive Collection Models

Machine learning analyzes debtor profiles, payment history, and behavioral patterns to determine the most effective recovery strategy.

By predicting the likelihood of repayment, businesses can focus resources where they yield the highest returns.

Rifa AI streamlines third-party negotiations, optimizes revenue-sharing agreements, and enhances recovery through AI-driven mediation. With predictive analytics, collection costs reduce by over 50%, ensuring businesses recover debts efficiently and ethically.

Collect Faster and Spend Less with Rifa AI

As regulations tighten and customer expectations evolve, businesses need an agile, compliant, and scalable debt collection strategy. The right technology can balance business efficiency with customer fairness, ensuring compliance and long-term trust.

Debt collection requires a careful balance of efficiency, compliance, and customer experience—Rifa AI delivers on all three. Rifa AI provides a scalable, AI-driven collection solution that evolves with business needs. From startups to enterprises, our automated outreach, intelligent risk analysis, and self-service portals ensure consistent, cost-effective recovery.

Rifa AI automates 10,000+ calls daily, delivering personalized payment reminders, automated dispute resolution, and seamless CRM updates. Our AI ensures 15%+ right-party contact rates, 5.2-minute call handling times, and zero compliance issues, outperforming industry standards.

Schedule a demo today and see how Rifa AI can cut collection costs by 50%+ while boosting recovery rates.

Mar 25, 2025

Mar 25, 2025

Mar 25, 2025

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved