How Debt Collection Agencies Report to Credit Bureaus

How Debt Collection Agencies Report to Credit Bureaus

How Debt Collection Agencies Report to Credit Bureaus

How Debt Collection Agencies Report to Credit Bureaus

Anant Sharma

Anant Sharma

Anant Sharma

Navigating debt can feel overwhelming for your customers, particularly when credit reports enter the picture. A common concern is, "Do collection agencies report to credit bureaus?" – a question many face.

This query is crucial as it directly impacts your customer’s financial well-being. According to the Consumer Financial Protection Bureau (CFPB), as of 2023, approximately 73 million Americans had debts in collections in the U.S. Understanding how to interact with credit bureaus is essential for managing your customer’s financial health.

In this blog, we'll break down how you can report to credit bureaus, the impact this has on your customer’s credit score, and how to manage these situations. Understanding this procedure will help you make informed judgments on how to manage debt collection.

To comprehend how debt collection agencies impact credit reports, it's essential to first explore the role of credit bureaus and how they manage financial information.

What are Credit Bureaus and Their Functions?

Credit bureaus (also called credit reporting agencies) collect and maintain consumer credit data. The three primary bureaus in the U.S. are Equifax, Experian, and TransUnion. These organizations rely on timely data from lenders and collection agencies to generate accurate credit reports.

Your agency plays a key role in shaping a consumer’s credit profile. Once an account is placed in collections, that information may be reported to these bureaus. The credit report will typically include:

Outstanding collection accounts

Dates of delinquency

Payment status updates

Each of these entries can influence the consumer’s credit score. Automating this process with Rifa AI ensures accurate reporting, reduces manual data handling, and avoids compliance issues that arise from reporting errors.

Now that you know the purpose of credit bureaus, let’s discuss the specific circumstances under which you can report your debt to these bureaus.

When Can You Report a Debt to the Credit Bureaus?

Debt collection agencies are legally permitted to report unpaid debts to credit bureaus—but only when specific conditions are met. Accurate and timely reporting is critical for maintaining compliance and preserving trust with both consumers and credit reporting agencies (CRAs). Reporting too early or without proper documentation can expose your agency to legal liability, consumer disputes, and regulatory scrutiny.

Here’s a breakdown of what needs to be in place before your agency submits a debt to a credit bureau:

1. The Debt Must Be Validated and Delinquent

Before reporting, agencies must ensure that the debt is both legitimate and delinquent:

Delinquency Timeline: Most debts must be at least 30 days past due to be considered delinquent. However, many agencies wait until the 90-day mark to reduce the risk of premature reporting.

Validation Requirement: Under the Fair Debt Collection Practices Act (FDCPA) and FCRA, the debt must be validated. This includes:

The name of the original creditor

The total amount owed

The date of delinquency

A breakdown of any interest, fees, or penalties

Rifa AI automates debt validation workflows, ensuring that only eligible accounts are flagged for reporting and that supporting documentation is stored for compliance audits.

2. The Debtor Must Be Notified

Regulatory frameworks require you to inform the consumer before the debt is reported. This notification must:

Include a 30-day dispute window (Validation Notice)

Outline the total balance and the original creditor

Clearly state that the account may be reported to credit bureaus if left unresolved

Failing to notify the debtor properly is a top cause of bureau disputes and CFPB complaints.

3. You Must Wait the Appropriate Timeframe

Even after notifying the debtor, you cannot report the debt immediately. The FCRA mandates a reasonable waiting period (commonly 30 days) to give the debtor an opportunity to dispute or pay the debt.

During this period:

All disputes must be addressed and resolved before reporting

If a consumer provides proof of payment or an error, you are obligated to remove or correct the record before submission

Rifa AI automatically pauses reporting during dispute periods, and flags accounts for human review when additional action is required.

4. You Must Follow Metro 2 Reporting Standards

Most credit bureaus require agencies to submit data using the Metro 2 format, a standardized file format developed by the Consumer Data Industry Association (CDIA). This format ensures consistency in reporting key data fields like:

Account status (open, closed, charged off, etc.)

Payment history

Balance details

Date of first delinquency (DOFD)

Agencies not following Metro 2 risk their data being rejected—or worse, inaccurately reflected in consumer credit reports.

5. The Debt Must Not Be Time-Barred

Agencies must also confirm that the debt is not past the statute of limitations in the state where the consumer resides. Even if a time-barred debt can be collected (in some cases), it typically cannot be reported to credit bureaus.

Statutes of limitations vary by state and debt type (e.g., credit cards vs. medical debt), ranging from 3 to 10 years. Rifa AI includes built-in rules engines that flag time-barred accounts automatically, reducing your risk of illegal reporting.

6. Only Report When It’s Operationally Justified

While you're legally permitted to report eligible debts, you’re not obligated to report everything. Agencies often create internal thresholds to avoid over-reporting:

Minimum balance requirements (e.g., only report debts over $100)

Client-specific policies (some creditors may prohibit bureau reporting)

Risk scoring (some accounts may not justify the cost of negative reporting)

Supercharge your debt collection with Rifa's AI automation capabilities: streamline 70% of workflows, achieve 99% accuracy, and save over 200 hours weekly—no API integration needed. Deploy in days and slash costs by up to 70%. Ready for transformation? Let Rifa AI lead the way to success.

Once your customer’s debt reaches the point of receiving a visit request from a collection agency, it’s important to understand the immediate steps and implications that follow.

What Happens When Your Customer Receives a Visit Request From a Collections Agency?

Once your agency takes over an account, the following steps are typically triggered:

Debtor Notification: A formal letter is issued detailing the amount owed, the original creditor, and their rights under the FDCPA.

Validation Window: Consumers are given 30 days to dispute the debt.

Bureau Reporting: If the debt is valid and remains unpaid, it can then be reported to credit bureaus.

Negotiation or Legal Action: Depending on internal policies, your agency may offer payment plans, settlements, or escalate to litigation.

At each step, Rifa AI can automate communication workflows, flag disputes, and ensure all actions remain compliant with state and federal regulations.

Sending a customer’s debt to a collection agency can have serious financial consequences, affecting their credit and ability to secure future loans or credit. Rifa AI provides data insights that ensure consistent and accurate reporting while maintaining compliance with regulations.

As your clients’ debt moves into the collections phase, it’s important to recognize the lasting effects and how this impacts their entire credit report.

How Will Debt Collection Affect Credit Scores and Reports?

Debt collection has far-reaching implications for both consumers and businesses. As a debt collection agency, understanding how your reporting actions impact credit scores and credit reports is essential. Not only does it affect the debtors' creditworthiness, but it also influences the actions your agency can take to recover debt effectively while staying compliant with credit reporting standards.

Negative Impact on Credit Score

When a debt is handed over to a collection agency, it is reported as a collection account to the major credit bureaus (Equifax, Experian, and TransUnion). This type of entry is considered a negative item on the debtor's credit report. The more recent the collection entry, the greater the negative impact on the debtor’s credit score.

Score Decrease: In some cases, a collection entry can cause a drop of 50–100 points or more in a consumer's credit score, depending on factors like the debtor's credit history and the recency of the delinquency. The more recent a collection entry, the greater the damage to a consumer’s credit score, and consequently, the harder it becomes for them to secure new credit in the future.

Impact on Creditworthiness: Lenders, landlords, and other financial entities view collection accounts as signals of a potential risk. A collection entry severely reduces the chances of future loan approvals, credit cards, or even certain employment opportunities that require credit checks.

Collection Account on Credit Report

Once the debt is reported, the entry remains on the debtor’s credit report for up to seven years. This means that even if the debt is settled or partially paid off, it will continue to reflect negatively on the debtor’s credit report until the seven-year period ends.

Long-Term Financial Consequences: For debt collection agencies, this long-term effect presents both an opportunity and a challenge. While it may improve recovery rates in the short term by forcing debtors to face the consequences of their actions, the long-term presence of the collection account can limit the debtor’s ability to obtain future credit, potentially leading to customer dissatisfaction.

Impact After Debt Settlement

Even after a debt is fully paid or settled, the collection entry will remain on the consumer's credit report as a "paid collection." Though paying off the debt may prevent further collection actions or lawsuits, it does not immediately improve the consumer’s credit score.

This can create challenges for your agency, as debtors might expect their credit scores to improve right after settlement. With Rifa AI’s tools, you can keep consumers informed about how paying off the debt won’t immediately raise their score, but it helps avoid further damaging actions like legal proceedings or wage garnishments. Additionally, educating clients about the settlement can improve customer relations.

Roles and Responsibilities of a Debt Collection Agency

As a debt collection agency, you have specific responsibilities to both your clients and the debtors you are collecting from. Ensuring compliance with federal and state laws is critical, particularly with laws like the Fair Debt Collection Practices Act (FDCPA). These rules help protect consumers from unethical debt collection practices while giving you the framework you need to collect debt legally and efficiently.

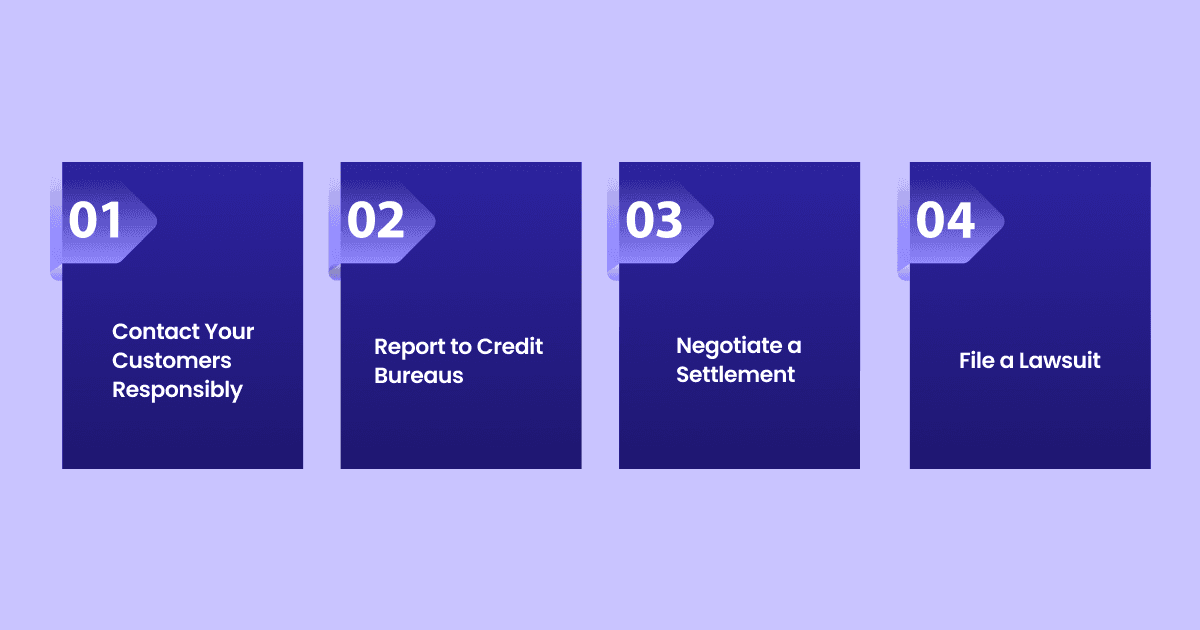

1. Contact Your Customers Responsibly

Under the FDCPA, you have the right to contact debtors, but there are clear guidelines regarding how and when you can do so. Your agency can contact debtors via:

Phone calls

Emails

Physical mail

However, these communications must not be harassing, deceptive, or abusive. Debt collectors are prohibited from calling at unreasonable hours, threatening violence, or using foul language. Ensuring these guidelines are met is vital for your agency's reputation and avoiding legal repercussions.

Rifa AI supports compliance by offering automated communication templates that ensure all outreach is compliant with the FDCPA and reduces human error.

2. Report to Credit Bureaus

When a debt remains unpaid, collection agencies have the option to report the debt to credit bureaus. This action can damage the debtor's credit score, but it is also a powerful tool for ensuring repayment.

Reporting Timeliness: It is essential that reporting to credit bureaus is done accurately and in a timely manner. With Rifa AI, your agency can automate monthly reporting to ensure consistent updates to credit bureaus, reducing manual errors and ensuring compliance with Metro 2 format reporting.

Impact on Credit Scores: As previously discussed, reporting to credit bureaus will likely have a negative impact on the debtor’s credit score. The sooner the debt is reported, the sooner it will affect the consumer’s score, pushing them toward resolution.

3. Negotiate a Settlement

Many collection agencies offer settlement options to debtors. Settling the debt for a reduced amount can help prevent further damage to the consumer's credit report, though the collection account will still remain on the report.

Settlements are an excellent way to reach a compromise between the debtor and your agency. Rifa AI helps automate the negotiation process by analyzing past payment histories and predicting the likelihood of successful settlements. The platform also tracks all communications and settlements to ensure transparency and compliance.

4. File a Lawsuit

If the debt is substantial and other efforts to recover it fail, a collection agency may file a lawsuit. If the court rules in favor of the creditor, the agency may be able to garnish the debtor's wages or seize assets to recover the owed amount.

Legal Actions: Lawsuits are typically seen as a last resort in debt collection, due to their cost and potential to escalate the situation. However, for larger debts, they can be a necessary tool for recovery.

Rifa AI aids in the preparation for legal action by ensuring that all necessary documentation is organized and ready for submission. This helps reduce delays and enhances your agency's ability to take swift legal action if necessary.

Conclusion

Understanding how debt collection agencies report to credit bureaus is crucial for both managing credit risk and maintaining strong customer relationships. The process is not without its challenges, but with the right tools, you can enhance your reporting efficiency, maintain compliance, and ultimately improve debt recovery outcomes.

Rifa AI offers an efficient, cost-effective, and personalized solution to optimize your collections and improve customer satisfaction. By automating your reporting processes, streamlining communication, and ensuring compliance with the latest regulations, Rifa AI helps your agency:

Report to credit bureaus accurately and efficiently

Manage disputes and settlements more effectively

Reduce operational costs and manual errors

With real-time data processing, seamless omnichannel integration, and a fully compliant automated system, Rifa AI is your trusted partner in debt recovery and other financial operations.

Don’t let overdue payments stop you from achieving your business goals. Schedule a demo today to learn how Rifa AI can revolutionize your financial operations and lead to significant cost savings.

Navigating debt can feel overwhelming for your customers, particularly when credit reports enter the picture. A common concern is, "Do collection agencies report to credit bureaus?" – a question many face.

This query is crucial as it directly impacts your customer’s financial well-being. According to the Consumer Financial Protection Bureau (CFPB), as of 2023, approximately 73 million Americans had debts in collections in the U.S. Understanding how to interact with credit bureaus is essential for managing your customer’s financial health.

In this blog, we'll break down how you can report to credit bureaus, the impact this has on your customer’s credit score, and how to manage these situations. Understanding this procedure will help you make informed judgments on how to manage debt collection.

To comprehend how debt collection agencies impact credit reports, it's essential to first explore the role of credit bureaus and how they manage financial information.

What are Credit Bureaus and Their Functions?

Credit bureaus (also called credit reporting agencies) collect and maintain consumer credit data. The three primary bureaus in the U.S. are Equifax, Experian, and TransUnion. These organizations rely on timely data from lenders and collection agencies to generate accurate credit reports.

Your agency plays a key role in shaping a consumer’s credit profile. Once an account is placed in collections, that information may be reported to these bureaus. The credit report will typically include:

Outstanding collection accounts

Dates of delinquency

Payment status updates

Each of these entries can influence the consumer’s credit score. Automating this process with Rifa AI ensures accurate reporting, reduces manual data handling, and avoids compliance issues that arise from reporting errors.

Now that you know the purpose of credit bureaus, let’s discuss the specific circumstances under which you can report your debt to these bureaus.

When Can You Report a Debt to the Credit Bureaus?

Debt collection agencies are legally permitted to report unpaid debts to credit bureaus—but only when specific conditions are met. Accurate and timely reporting is critical for maintaining compliance and preserving trust with both consumers and credit reporting agencies (CRAs). Reporting too early or without proper documentation can expose your agency to legal liability, consumer disputes, and regulatory scrutiny.

Here’s a breakdown of what needs to be in place before your agency submits a debt to a credit bureau:

1. The Debt Must Be Validated and Delinquent

Before reporting, agencies must ensure that the debt is both legitimate and delinquent:

Delinquency Timeline: Most debts must be at least 30 days past due to be considered delinquent. However, many agencies wait until the 90-day mark to reduce the risk of premature reporting.

Validation Requirement: Under the Fair Debt Collection Practices Act (FDCPA) and FCRA, the debt must be validated. This includes:

The name of the original creditor

The total amount owed

The date of delinquency

A breakdown of any interest, fees, or penalties

Rifa AI automates debt validation workflows, ensuring that only eligible accounts are flagged for reporting and that supporting documentation is stored for compliance audits.

2. The Debtor Must Be Notified

Regulatory frameworks require you to inform the consumer before the debt is reported. This notification must:

Include a 30-day dispute window (Validation Notice)

Outline the total balance and the original creditor

Clearly state that the account may be reported to credit bureaus if left unresolved

Failing to notify the debtor properly is a top cause of bureau disputes and CFPB complaints.

3. You Must Wait the Appropriate Timeframe

Even after notifying the debtor, you cannot report the debt immediately. The FCRA mandates a reasonable waiting period (commonly 30 days) to give the debtor an opportunity to dispute or pay the debt.

During this period:

All disputes must be addressed and resolved before reporting

If a consumer provides proof of payment or an error, you are obligated to remove or correct the record before submission

Rifa AI automatically pauses reporting during dispute periods, and flags accounts for human review when additional action is required.

4. You Must Follow Metro 2 Reporting Standards

Most credit bureaus require agencies to submit data using the Metro 2 format, a standardized file format developed by the Consumer Data Industry Association (CDIA). This format ensures consistency in reporting key data fields like:

Account status (open, closed, charged off, etc.)

Payment history

Balance details

Date of first delinquency (DOFD)

Agencies not following Metro 2 risk their data being rejected—or worse, inaccurately reflected in consumer credit reports.

5. The Debt Must Not Be Time-Barred

Agencies must also confirm that the debt is not past the statute of limitations in the state where the consumer resides. Even if a time-barred debt can be collected (in some cases), it typically cannot be reported to credit bureaus.

Statutes of limitations vary by state and debt type (e.g., credit cards vs. medical debt), ranging from 3 to 10 years. Rifa AI includes built-in rules engines that flag time-barred accounts automatically, reducing your risk of illegal reporting.

6. Only Report When It’s Operationally Justified

While you're legally permitted to report eligible debts, you’re not obligated to report everything. Agencies often create internal thresholds to avoid over-reporting:

Minimum balance requirements (e.g., only report debts over $100)

Client-specific policies (some creditors may prohibit bureau reporting)

Risk scoring (some accounts may not justify the cost of negative reporting)

Supercharge your debt collection with Rifa's AI automation capabilities: streamline 70% of workflows, achieve 99% accuracy, and save over 200 hours weekly—no API integration needed. Deploy in days and slash costs by up to 70%. Ready for transformation? Let Rifa AI lead the way to success.

Once your customer’s debt reaches the point of receiving a visit request from a collection agency, it’s important to understand the immediate steps and implications that follow.

What Happens When Your Customer Receives a Visit Request From a Collections Agency?

Once your agency takes over an account, the following steps are typically triggered:

Debtor Notification: A formal letter is issued detailing the amount owed, the original creditor, and their rights under the FDCPA.

Validation Window: Consumers are given 30 days to dispute the debt.

Bureau Reporting: If the debt is valid and remains unpaid, it can then be reported to credit bureaus.

Negotiation or Legal Action: Depending on internal policies, your agency may offer payment plans, settlements, or escalate to litigation.

At each step, Rifa AI can automate communication workflows, flag disputes, and ensure all actions remain compliant with state and federal regulations.

Sending a customer’s debt to a collection agency can have serious financial consequences, affecting their credit and ability to secure future loans or credit. Rifa AI provides data insights that ensure consistent and accurate reporting while maintaining compliance with regulations.

As your clients’ debt moves into the collections phase, it’s important to recognize the lasting effects and how this impacts their entire credit report.

How Will Debt Collection Affect Credit Scores and Reports?

Debt collection has far-reaching implications for both consumers and businesses. As a debt collection agency, understanding how your reporting actions impact credit scores and credit reports is essential. Not only does it affect the debtors' creditworthiness, but it also influences the actions your agency can take to recover debt effectively while staying compliant with credit reporting standards.

Negative Impact on Credit Score

When a debt is handed over to a collection agency, it is reported as a collection account to the major credit bureaus (Equifax, Experian, and TransUnion). This type of entry is considered a negative item on the debtor's credit report. The more recent the collection entry, the greater the negative impact on the debtor’s credit score.

Score Decrease: In some cases, a collection entry can cause a drop of 50–100 points or more in a consumer's credit score, depending on factors like the debtor's credit history and the recency of the delinquency. The more recent a collection entry, the greater the damage to a consumer’s credit score, and consequently, the harder it becomes for them to secure new credit in the future.

Impact on Creditworthiness: Lenders, landlords, and other financial entities view collection accounts as signals of a potential risk. A collection entry severely reduces the chances of future loan approvals, credit cards, or even certain employment opportunities that require credit checks.

Collection Account on Credit Report

Once the debt is reported, the entry remains on the debtor’s credit report for up to seven years. This means that even if the debt is settled or partially paid off, it will continue to reflect negatively on the debtor’s credit report until the seven-year period ends.

Long-Term Financial Consequences: For debt collection agencies, this long-term effect presents both an opportunity and a challenge. While it may improve recovery rates in the short term by forcing debtors to face the consequences of their actions, the long-term presence of the collection account can limit the debtor’s ability to obtain future credit, potentially leading to customer dissatisfaction.

Impact After Debt Settlement

Even after a debt is fully paid or settled, the collection entry will remain on the consumer's credit report as a "paid collection." Though paying off the debt may prevent further collection actions or lawsuits, it does not immediately improve the consumer’s credit score.

This can create challenges for your agency, as debtors might expect their credit scores to improve right after settlement. With Rifa AI’s tools, you can keep consumers informed about how paying off the debt won’t immediately raise their score, but it helps avoid further damaging actions like legal proceedings or wage garnishments. Additionally, educating clients about the settlement can improve customer relations.

Roles and Responsibilities of a Debt Collection Agency

As a debt collection agency, you have specific responsibilities to both your clients and the debtors you are collecting from. Ensuring compliance with federal and state laws is critical, particularly with laws like the Fair Debt Collection Practices Act (FDCPA). These rules help protect consumers from unethical debt collection practices while giving you the framework you need to collect debt legally and efficiently.

1. Contact Your Customers Responsibly

Under the FDCPA, you have the right to contact debtors, but there are clear guidelines regarding how and when you can do so. Your agency can contact debtors via:

Phone calls

Emails

Physical mail

However, these communications must not be harassing, deceptive, or abusive. Debt collectors are prohibited from calling at unreasonable hours, threatening violence, or using foul language. Ensuring these guidelines are met is vital for your agency's reputation and avoiding legal repercussions.

Rifa AI supports compliance by offering automated communication templates that ensure all outreach is compliant with the FDCPA and reduces human error.

2. Report to Credit Bureaus

When a debt remains unpaid, collection agencies have the option to report the debt to credit bureaus. This action can damage the debtor's credit score, but it is also a powerful tool for ensuring repayment.

Reporting Timeliness: It is essential that reporting to credit bureaus is done accurately and in a timely manner. With Rifa AI, your agency can automate monthly reporting to ensure consistent updates to credit bureaus, reducing manual errors and ensuring compliance with Metro 2 format reporting.

Impact on Credit Scores: As previously discussed, reporting to credit bureaus will likely have a negative impact on the debtor’s credit score. The sooner the debt is reported, the sooner it will affect the consumer’s score, pushing them toward resolution.

3. Negotiate a Settlement

Many collection agencies offer settlement options to debtors. Settling the debt for a reduced amount can help prevent further damage to the consumer's credit report, though the collection account will still remain on the report.

Settlements are an excellent way to reach a compromise between the debtor and your agency. Rifa AI helps automate the negotiation process by analyzing past payment histories and predicting the likelihood of successful settlements. The platform also tracks all communications and settlements to ensure transparency and compliance.

4. File a Lawsuit

If the debt is substantial and other efforts to recover it fail, a collection agency may file a lawsuit. If the court rules in favor of the creditor, the agency may be able to garnish the debtor's wages or seize assets to recover the owed amount.

Legal Actions: Lawsuits are typically seen as a last resort in debt collection, due to their cost and potential to escalate the situation. However, for larger debts, they can be a necessary tool for recovery.

Rifa AI aids in the preparation for legal action by ensuring that all necessary documentation is organized and ready for submission. This helps reduce delays and enhances your agency's ability to take swift legal action if necessary.

Conclusion

Understanding how debt collection agencies report to credit bureaus is crucial for both managing credit risk and maintaining strong customer relationships. The process is not without its challenges, but with the right tools, you can enhance your reporting efficiency, maintain compliance, and ultimately improve debt recovery outcomes.

Rifa AI offers an efficient, cost-effective, and personalized solution to optimize your collections and improve customer satisfaction. By automating your reporting processes, streamlining communication, and ensuring compliance with the latest regulations, Rifa AI helps your agency:

Report to credit bureaus accurately and efficiently

Manage disputes and settlements more effectively

Reduce operational costs and manual errors

With real-time data processing, seamless omnichannel integration, and a fully compliant automated system, Rifa AI is your trusted partner in debt recovery and other financial operations.

Don’t let overdue payments stop you from achieving your business goals. Schedule a demo today to learn how Rifa AI can revolutionize your financial operations and lead to significant cost savings.

Mar 27, 2025

Mar 27, 2025

Mar 27, 2025

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved