What is Credit Management and Why It Matters

What is Credit Management and Why It Matters

What is Credit Management and Why It Matters

What is Credit Management and Why It Matters

Anant Sharma

Anant Sharma

Anant Sharma

What is Credit Management and Why It Matters?

Effective cash flow management is crucial for any business, and having the financial agility to adapt to changing circumstances is key. In this context, credit management becomes more than just an administrative task—it's a strategic imperative. According to industry reports from 2022, businesses with robust credit management practices experience a 0.16% average bad debt-to-sales ratio.

That said, credit management plays a vital role in maintaining financial stability and driving long-term success. Whether you're a business owner analyzing changing market conditions or a financial professional focused on minimizing risks, grasping the key aspects of credit management is essential. Understanding these fundamentals helps ensure your business stays on solid financial ground, no matter what challenges arise.

This blog will guide you through the concept of credit management, explain why it matters, and offer actionable insights to improve the process.

What is Credit Management?

Credit management refers to the strategies and processes you can use to oversee and control credit-related activities. In a business context, it includes managing customer credit accounts, assessing credit risk, setting payment terms, and ensuring prompt payment collection. Credit management aims to balance maintaining healthy cash flow and minimizing the risks of offering credit.

The process involves evaluating your potential customers or clients before extending credit, setting clear credit terms, monitoring outstanding accounts, and taking corrective action when necessary. By actively managing credit, you can reduce the chances of bad debts negatively affecting financial performance.

Now that we clearly understand what credit management is, let's explore the various contexts in which it is applied to ensure financial stability and growth.

What Situations Make Credit Management Useful?

Credit management is primarily used in business contexts. Here’s a breakdown of where it’s commonly used:

Businesses Offering Credit to Customers: If your company provides goods or services on credit, then you must manage your customer accounts efficiently. You need to assess the financial health of your customers, determine appropriate credit limits, and set clear payment terms. Managing overdue accounts and ensuring timely collections is also vital.

Supplier and Vendor Relationships: Companies often extend credit to suppliers or vendors, allowing them to purchase goods or services with deferred payments. In these situations, credit management helps ensure that your business isn’t overexposed to risk. You can avoid issues such as missed payments or over-leveraging credit by carefully reviewing supplier terms and continuously monitoring the accounts payable balance.

Financial Institutions: Banks and other financial institutions use credit management processes to assess the creditworthiness of borrowers, such as when they issue loans or extend lines of credit. They apply rigorous credit reviews and risk assessments to minimize lending risks. Rifa AI’s collections and risk assessment features can predict potential defaults and reduce operational costs without API integration.

Importance of Credit Management

Credit management is important because it ensures that your business remains healthy and sustainable. For businesses, poor credit management can lead to bad debt, which eats into profits and may lead to liquidity problems.

By having a solid credit management strategy, you improve your cash flow, reduce the risk of non-payment, and enhance customer satisfaction. With strong credit management, you will be in a position to extend credit to trustworthy customers, encouraging growth and fostering loyalty.

With the importance of credit management in mind, let’s break down the steps involved in effectively managing credit to help you achieve the desired financial outcomes.

The Steps in the Credit Management Process

Effective credit management is essential for minimizing risk, maintaining healthy cash flow, and ensuring business growth. The process involves several important steps, each designed to evaluate, monitor, and maintain the financial stability of the credit system. Below is a breakdown of the steps involved in credit management:

1. Credit Policy Development

The foundation of any successful credit management strategy is a well-defined credit policy. This policy sets the rules and guidelines for granting, monitoring, and collecting credit. A clear credit policy establishes consistency and helps manage customer expectations.

Your credit policy should address several core aspects:

Eligibility Criteria: Define the specific conditions under which your customers will be eligible for credit, including their financial stability, industry standing, and previous credit history.

Payment Terms: Specify the terms of payment (e.g., net 30, 60, or 90 days) and conditions under which exceptions may be made.

Credit Limits: Establish rules for setting credit limits, considering customer history, industry type, and the risk tolerance of your business.

Overdue Payment Procedures: Outline how overdue payments you will handle, including the steps taken to follow up and escalate any issues.

Discounts and Incentives: Establish rules for providing discounts for early payments or other rewards to promote on-time payments.

A structured credit policy helps streamline the decision-making process and ensures that customers meeting your business's risk standards receive credit.

2. Credit Assessment

Before extending credit to any customer, it’s essential to thoroughly assess their financial situation to determine their ability to repay. This assessment typically involves reviewing several key pieces of information, such as the customer's credit history, financial statements, and other relevant data.

Credit History: Check the customer’s past payment history, including any defaults, bankruptcies, or liens, by obtaining a credit report from a reliable credit analysis agency.

Financial Stability: Review financial documents, including balance sheets, income statements, and tax filings, to evaluate the client's financial condition.

Additional Factors: Consider external factors such as industry risk, economic conditions, and the company’s market standing.

Rifa AI can automate this process by analyzing large volumes of data in real-time, providing you with an accurate assessment of creditworthiness quickly. AI-powered tools can evaluate customer data, including payment history and cash flow, reducing manual effort and speeding up decision-making.

3. Credit Approval and Terms Setting

Once the credit assessment is complete, you need to make a decision on whether to approve the credit application and what terms to offer. This includes setting the credit limit, establishing the payment terms, and specifying any penalties for late payments.

Key steps include:

Approval Decision: If the customer meets the necessary criteria, you approve the credit request. If they don’t meet the criteria, consider requesting payment in advance or applying more stringent terms.

Setting Credit Limits: Establish a credit limit based on the customer’s financial profile and business history. For new customers, it’s often advisable to set a lower limit and increase it gradually as they build a solid payment record.

Terms Agreement: Clearly outline the payment terms, including due dates, interest rates for overdue payments, and any discounts for early payments

Rifa AI helps you automate the process of setting credit terms by analyzing customer data and suggesting optimal credit limits based on predictive analytics. This ensures that you set appropriate limits aligned with the customer’s financial behavior.

4. Ongoing Monitoring

After extending credit, continuous monitoring of customer accounts is crucial. Monitoring helps identify potential payment issues before they become significant problems, ensuring that the business can take timely action.

Ongoing monitoring includes:

Tracking Payment Behavior: Regularly review customer payment history to spot patterns or delays that could indicate cash flow issues.

Regular Credit Reviews: Conduct periodic reviews of customer credit to ensure there is no significant change in their financial situation. You must update credit limits or terms accordingly.

Communication with Customers: Maintain regular communication with customers to make sure they understand their payment timelines and to resolve any issues before they worsen.

Rifa AI can assist in this process by automating account monitoring. It can flag potential late payments, send automated reminders, and alert you when a customer’s creditworthiness begins to decline. This enables you to act quickly and prevent overdue payments.

5. Collections and Dispute Resolution

A well-defined collection process is necessary for customers who fail to make timely payments. Effective collections and dispute resolution practices minimize bad debt and ensure you handle disputes efficiently.

Steps in the collection process include:

Reminder Notifications: Begin by sending automated reminders as soon as payments are overdue. Clear communication about the overdue status can prompt customers to pay before you take any further action.

Negotiating Payment Plans: For clients facing financial challenges, think about providing payment options and settling the debt in smaller, more manageable installments.

Escalation to Legal Channels: If all efforts fail, you can escalate the issue to legal proceedings or third-party collections agencies to recover the debt.

With automated collections tools, you can reduce the time and effort spent managing overdue accounts. The platform can send reminders, help negotiate payment terms, and even automate the escalation of issues, ensuring that the collection process is efficient and systematic.

By following these steps, you can better manage credit, ensure prompt payments, and maintain financial stability. Now that we’ve covered the process, let’s discuss the tangible benefits of maintaining a solid credit management strategy.

The Benefits of Good Credit Management

When done correctly, credit management can bring numerous benefits to your business. Here are the primary advantages:

Improved Cash Flow: By ensuring timely payments, you maintain a steady inflow of cash, which is essential for operational activities, payroll, and other expenses.

Reduced Risk of Bad Debts: A strong credit management process helps identify high-risk customers early, reducing the possibility of non-payment and mitigating potential losses.

Enhanced Customer Relationships: Clear and consistent credit terms foster trust between you and your customers. It’s also easier to manage and communicate expectations when both parties understand the agreed-upon terms. Rifa AI can communicate with customers through automated notifications and reminders, maintaining positive relationships while ensuring on-time payments.

Better Financial Decision-Making: Having a clear understanding of your credit situation allows for more informed decisions. It helps in forecasting cash flow, budgeting, and making strategic investments.

Stronger Creditworthiness: Maintaining a solid credit history makes it easier for your organization to get future loans or advantageous financial arrangements. It demonstrates financial responsibility and enhances credibility.

Therefore, embracing effective credit management isn't just about minimizing risk; it's about identifying opportunities for growth, stability, and sustained financial success. Examining the key factors that influence the credit review and risk analysis process is important to better understand how to navigate credit management.

Rifa AI’s automation can help you increase debt collection by streamlining 70% of procedures, achieving 99% accuracy, and saving over 200 hours per week without requiring API interaction. Reduce expenses by up to 70% and deploy in a matter of days. Are you prepared to change? Allow Rifa AI to guide you to success.

Factors Influencing the Credit Review and Risk Analysis Process

Several factors influence the credit review and risk analysis process. These elements help you assess the potential risks of lending and determine whether a customer is likely to repay credit extended to them. Here are the key factors:

Credit History: A customer’s past behavior regarding credit is one of the most significant indicators of their future creditworthiness. You can review an individual or company’s credit reports, paying attention to previous late payments or defaults.

Financial Stability: You can assess the financial health of a customer by examining financial statements, revenue, profit margins, and other economic indicators. The more stable and profitable a business or individual is, the more likely they are to repay debts.

Payment Behavior: You should track a customer’s payment history, including whether they make payments on time or if there’s a pattern of late payments.

Industry Risks: Some industries are more prone to volatility, which may affect customers’ ability to pay. Volatility refers to the degree of variation in the price or value of an asset, product, or market over time. In the business context, it usually manifests through unpredictable fluctuations in demand, market conditions, or external economic factors. You should factor in industry trends, economic forecasts, and potential risks specific to that sector.

Economic Conditions: Broader economic factors, such as inflation rates, interest rates, and economic growth, can influence credit risk. In times of economic instability, your customers may face difficulty in repaying debts.

Consider these factors to better identify potential risks and make educated decisions about credit extension. As we move forward, let’s explore what qualities make a credit manager high-performing and essential to a successful credit management system.

The Qualities of an Effective Credit Manager

A high-performing credit manager is critical to the success of credit management. These individuals are responsible for overseeing credit policies, analyzing risk, and ensuring timely payments. Here are the key traits of an effective credit manager:

Attention to Detail: Successful credit managers pay close attention to the fine details of credit agreements, payment terms, and customer histories to ensure proper management.

Strong Analytical Skills: A good credit manager can analyze financial data, assess risk, and make strategic decisions based on the information available. Their ability to foresee potential issues before they arise is valuable.

Excellent Communication Skills: Credit managers must communicate effectively with both internal teams and customers. They should be able to negotiate terms, address concerns, and manage any disputes that arise professionally.

Risk Management Expertise: High-performing credit managers know how to assess and mitigate financial risks. They are skilled at identifying problem accounts early and taking corrective action.

Decisiveness and Leadership: A great credit manager makes timely and effective decisions. They lead by example, ensuring that the credit management team follows established procedures and maintains best practices.

What if you don’t need a credit manager when you can automate your workflow? With Rifa AI, simplify your credit risk assessments, collections, and compliance, all powered by cutting-edge automation. Automate 70% of your procedures, minimize human error and ensure real-time data accuracy.

Our advanced encryption safeguards sensitive financial data, and we comply with regulations like GDPR. Benefit from predictive analytics to optimize compliance and collections. Transform your processes, reduce costs, and achieve near-perfect accuracy in just days with Rifa AI.

Tips to Improve Your Credit Management Process

You can significantly enhance your cash flow, minimize bad debt, and foster stronger customer relationships by implementing strategic adjustments and utilizing modern tools. Let's explore actionable tips to elevate your credit management practices:

Establish Clear Credit Policies: A well-defined credit policy is key to reducing misunderstandings and ensuring consistency in decision-making. This policy should clearly outline the terms of credit, how you will collect payments, and what to do when payments are overdue.

Use Technology for Monitoring: Credit management tools and software can streamline the process, automate monitoring, and flag overdue payments, allowing you to act quickly and efficiently. Rifa AI can monitor customer accounts, flag overdue payments, and even automate follow-up communications, ensuring no account goes unnoticed.

Maintain Strong Customer Relationships: Open communication with customers is essential. Regularly checking in with customers about their payment schedules and offering flexible payment terms when needed can help prevent late payments. Rifa AI helps facilitate this by sending automated reminders through voice, chat and email, ensuring that your customers are always aware of payment deadlines.

With a solid understanding of the credit management process and its benefits, let’s now explore how AI automation can elevate your approach. It will make your business process even more efficient and strategic, particularly when it comes to managing late payments.

How AI Automation Can Help You Create a Strategic Credit Management Procedure for Late Payments

Artificial Intelligence (AI) and automation are revolutionizing credit management. Here’s how AI can simplify and enhance your credit management process:

Automates Key Aspects of Credit Management: AI can automate the review process, risk analysis, and collections, allowing you to efficiently manage customer credit accounts.

Real-Time Creditworthiness Assessment: AI-powered tools can assess a customer’s creditworthiness by analyzing vast amounts of data in real-time, helping you make informed decisions quickly.

Flagging Accounts at Risk of Late Payments: AI systems can automatically identify and flag accounts that are at risk of late payment, allowing you to take timely action.

Sending Automated Payment Reminders: AI tools can automatically send reminders to your customers about upcoming or overdue payments, reducing the possibility of missed payments.

Creating Custom Payment Plans: For overdue payments, AI can analyze a customer’s financial situation and suggest customized payment plans, improving the chances of recovering outstanding debts.

Reducing Human Error: Automating credit management minimizes the risk of human error, ensuring more accurate assessments and decisions.

Speeding Up the Process: AI accelerates the entire credit management process, enabling you to address overdue payments and credit issues faster.

Strategic Decision-Making: With AI, you can make more strategic and data-driven decisions, optimizing the credit management process and mitigating risks.

Incorporating AI into your credit management procedures can lead to better risk mitigation, fewer bad debts, and more efficient operations.

Conclusion

Credit management is a critical component of any financial operation for your business. By implementing effective credit management strategies, you can ensure timely payments, reduce bad debts, and maintain financial health.

With the right processes in place, along with modern tools such as AI automation, you can deal with the complexities of credit with greater ease. As you focus on improving your credit management practices, you’ll strengthen your financial position and set yourself up for long-term success.

Rifa AI offers an efficient, cost-effective, and personalized solution to streamline your collections and improve customer satisfaction. With real-time data processing, seamless omnichannel integration, and a fully compliant, automated system, Rifa AI is your trusted partner in debt recovery and other financial operations.

What is Credit Management and Why It Matters?

Effective cash flow management is crucial for any business, and having the financial agility to adapt to changing circumstances is key. In this context, credit management becomes more than just an administrative task—it's a strategic imperative. According to industry reports from 2022, businesses with robust credit management practices experience a 0.16% average bad debt-to-sales ratio.

That said, credit management plays a vital role in maintaining financial stability and driving long-term success. Whether you're a business owner analyzing changing market conditions or a financial professional focused on minimizing risks, grasping the key aspects of credit management is essential. Understanding these fundamentals helps ensure your business stays on solid financial ground, no matter what challenges arise.

This blog will guide you through the concept of credit management, explain why it matters, and offer actionable insights to improve the process.

What is Credit Management?

Credit management refers to the strategies and processes you can use to oversee and control credit-related activities. In a business context, it includes managing customer credit accounts, assessing credit risk, setting payment terms, and ensuring prompt payment collection. Credit management aims to balance maintaining healthy cash flow and minimizing the risks of offering credit.

The process involves evaluating your potential customers or clients before extending credit, setting clear credit terms, monitoring outstanding accounts, and taking corrective action when necessary. By actively managing credit, you can reduce the chances of bad debts negatively affecting financial performance.

Now that we clearly understand what credit management is, let's explore the various contexts in which it is applied to ensure financial stability and growth.

What Situations Make Credit Management Useful?

Credit management is primarily used in business contexts. Here’s a breakdown of where it’s commonly used:

Businesses Offering Credit to Customers: If your company provides goods or services on credit, then you must manage your customer accounts efficiently. You need to assess the financial health of your customers, determine appropriate credit limits, and set clear payment terms. Managing overdue accounts and ensuring timely collections is also vital.

Supplier and Vendor Relationships: Companies often extend credit to suppliers or vendors, allowing them to purchase goods or services with deferred payments. In these situations, credit management helps ensure that your business isn’t overexposed to risk. You can avoid issues such as missed payments or over-leveraging credit by carefully reviewing supplier terms and continuously monitoring the accounts payable balance.

Financial Institutions: Banks and other financial institutions use credit management processes to assess the creditworthiness of borrowers, such as when they issue loans or extend lines of credit. They apply rigorous credit reviews and risk assessments to minimize lending risks. Rifa AI’s collections and risk assessment features can predict potential defaults and reduce operational costs without API integration.

Importance of Credit Management

Credit management is important because it ensures that your business remains healthy and sustainable. For businesses, poor credit management can lead to bad debt, which eats into profits and may lead to liquidity problems.

By having a solid credit management strategy, you improve your cash flow, reduce the risk of non-payment, and enhance customer satisfaction. With strong credit management, you will be in a position to extend credit to trustworthy customers, encouraging growth and fostering loyalty.

With the importance of credit management in mind, let’s break down the steps involved in effectively managing credit to help you achieve the desired financial outcomes.

The Steps in the Credit Management Process

Effective credit management is essential for minimizing risk, maintaining healthy cash flow, and ensuring business growth. The process involves several important steps, each designed to evaluate, monitor, and maintain the financial stability of the credit system. Below is a breakdown of the steps involved in credit management:

1. Credit Policy Development

The foundation of any successful credit management strategy is a well-defined credit policy. This policy sets the rules and guidelines for granting, monitoring, and collecting credit. A clear credit policy establishes consistency and helps manage customer expectations.

Your credit policy should address several core aspects:

Eligibility Criteria: Define the specific conditions under which your customers will be eligible for credit, including their financial stability, industry standing, and previous credit history.

Payment Terms: Specify the terms of payment (e.g., net 30, 60, or 90 days) and conditions under which exceptions may be made.

Credit Limits: Establish rules for setting credit limits, considering customer history, industry type, and the risk tolerance of your business.

Overdue Payment Procedures: Outline how overdue payments you will handle, including the steps taken to follow up and escalate any issues.

Discounts and Incentives: Establish rules for providing discounts for early payments or other rewards to promote on-time payments.

A structured credit policy helps streamline the decision-making process and ensures that customers meeting your business's risk standards receive credit.

2. Credit Assessment

Before extending credit to any customer, it’s essential to thoroughly assess their financial situation to determine their ability to repay. This assessment typically involves reviewing several key pieces of information, such as the customer's credit history, financial statements, and other relevant data.

Credit History: Check the customer’s past payment history, including any defaults, bankruptcies, or liens, by obtaining a credit report from a reliable credit analysis agency.

Financial Stability: Review financial documents, including balance sheets, income statements, and tax filings, to evaluate the client's financial condition.

Additional Factors: Consider external factors such as industry risk, economic conditions, and the company’s market standing.

Rifa AI can automate this process by analyzing large volumes of data in real-time, providing you with an accurate assessment of creditworthiness quickly. AI-powered tools can evaluate customer data, including payment history and cash flow, reducing manual effort and speeding up decision-making.

3. Credit Approval and Terms Setting

Once the credit assessment is complete, you need to make a decision on whether to approve the credit application and what terms to offer. This includes setting the credit limit, establishing the payment terms, and specifying any penalties for late payments.

Key steps include:

Approval Decision: If the customer meets the necessary criteria, you approve the credit request. If they don’t meet the criteria, consider requesting payment in advance or applying more stringent terms.

Setting Credit Limits: Establish a credit limit based on the customer’s financial profile and business history. For new customers, it’s often advisable to set a lower limit and increase it gradually as they build a solid payment record.

Terms Agreement: Clearly outline the payment terms, including due dates, interest rates for overdue payments, and any discounts for early payments

Rifa AI helps you automate the process of setting credit terms by analyzing customer data and suggesting optimal credit limits based on predictive analytics. This ensures that you set appropriate limits aligned with the customer’s financial behavior.

4. Ongoing Monitoring

After extending credit, continuous monitoring of customer accounts is crucial. Monitoring helps identify potential payment issues before they become significant problems, ensuring that the business can take timely action.

Ongoing monitoring includes:

Tracking Payment Behavior: Regularly review customer payment history to spot patterns or delays that could indicate cash flow issues.

Regular Credit Reviews: Conduct periodic reviews of customer credit to ensure there is no significant change in their financial situation. You must update credit limits or terms accordingly.

Communication with Customers: Maintain regular communication with customers to make sure they understand their payment timelines and to resolve any issues before they worsen.

Rifa AI can assist in this process by automating account monitoring. It can flag potential late payments, send automated reminders, and alert you when a customer’s creditworthiness begins to decline. This enables you to act quickly and prevent overdue payments.

5. Collections and Dispute Resolution

A well-defined collection process is necessary for customers who fail to make timely payments. Effective collections and dispute resolution practices minimize bad debt and ensure you handle disputes efficiently.

Steps in the collection process include:

Reminder Notifications: Begin by sending automated reminders as soon as payments are overdue. Clear communication about the overdue status can prompt customers to pay before you take any further action.

Negotiating Payment Plans: For clients facing financial challenges, think about providing payment options and settling the debt in smaller, more manageable installments.

Escalation to Legal Channels: If all efforts fail, you can escalate the issue to legal proceedings or third-party collections agencies to recover the debt.

With automated collections tools, you can reduce the time and effort spent managing overdue accounts. The platform can send reminders, help negotiate payment terms, and even automate the escalation of issues, ensuring that the collection process is efficient and systematic.

By following these steps, you can better manage credit, ensure prompt payments, and maintain financial stability. Now that we’ve covered the process, let’s discuss the tangible benefits of maintaining a solid credit management strategy.

The Benefits of Good Credit Management

When done correctly, credit management can bring numerous benefits to your business. Here are the primary advantages:

Improved Cash Flow: By ensuring timely payments, you maintain a steady inflow of cash, which is essential for operational activities, payroll, and other expenses.

Reduced Risk of Bad Debts: A strong credit management process helps identify high-risk customers early, reducing the possibility of non-payment and mitigating potential losses.

Enhanced Customer Relationships: Clear and consistent credit terms foster trust between you and your customers. It’s also easier to manage and communicate expectations when both parties understand the agreed-upon terms. Rifa AI can communicate with customers through automated notifications and reminders, maintaining positive relationships while ensuring on-time payments.

Better Financial Decision-Making: Having a clear understanding of your credit situation allows for more informed decisions. It helps in forecasting cash flow, budgeting, and making strategic investments.

Stronger Creditworthiness: Maintaining a solid credit history makes it easier for your organization to get future loans or advantageous financial arrangements. It demonstrates financial responsibility and enhances credibility.

Therefore, embracing effective credit management isn't just about minimizing risk; it's about identifying opportunities for growth, stability, and sustained financial success. Examining the key factors that influence the credit review and risk analysis process is important to better understand how to navigate credit management.

Rifa AI’s automation can help you increase debt collection by streamlining 70% of procedures, achieving 99% accuracy, and saving over 200 hours per week without requiring API interaction. Reduce expenses by up to 70% and deploy in a matter of days. Are you prepared to change? Allow Rifa AI to guide you to success.

Factors Influencing the Credit Review and Risk Analysis Process

Several factors influence the credit review and risk analysis process. These elements help you assess the potential risks of lending and determine whether a customer is likely to repay credit extended to them. Here are the key factors:

Credit History: A customer’s past behavior regarding credit is one of the most significant indicators of their future creditworthiness. You can review an individual or company’s credit reports, paying attention to previous late payments or defaults.

Financial Stability: You can assess the financial health of a customer by examining financial statements, revenue, profit margins, and other economic indicators. The more stable and profitable a business or individual is, the more likely they are to repay debts.

Payment Behavior: You should track a customer’s payment history, including whether they make payments on time or if there’s a pattern of late payments.

Industry Risks: Some industries are more prone to volatility, which may affect customers’ ability to pay. Volatility refers to the degree of variation in the price or value of an asset, product, or market over time. In the business context, it usually manifests through unpredictable fluctuations in demand, market conditions, or external economic factors. You should factor in industry trends, economic forecasts, and potential risks specific to that sector.

Economic Conditions: Broader economic factors, such as inflation rates, interest rates, and economic growth, can influence credit risk. In times of economic instability, your customers may face difficulty in repaying debts.

Consider these factors to better identify potential risks and make educated decisions about credit extension. As we move forward, let’s explore what qualities make a credit manager high-performing and essential to a successful credit management system.

The Qualities of an Effective Credit Manager

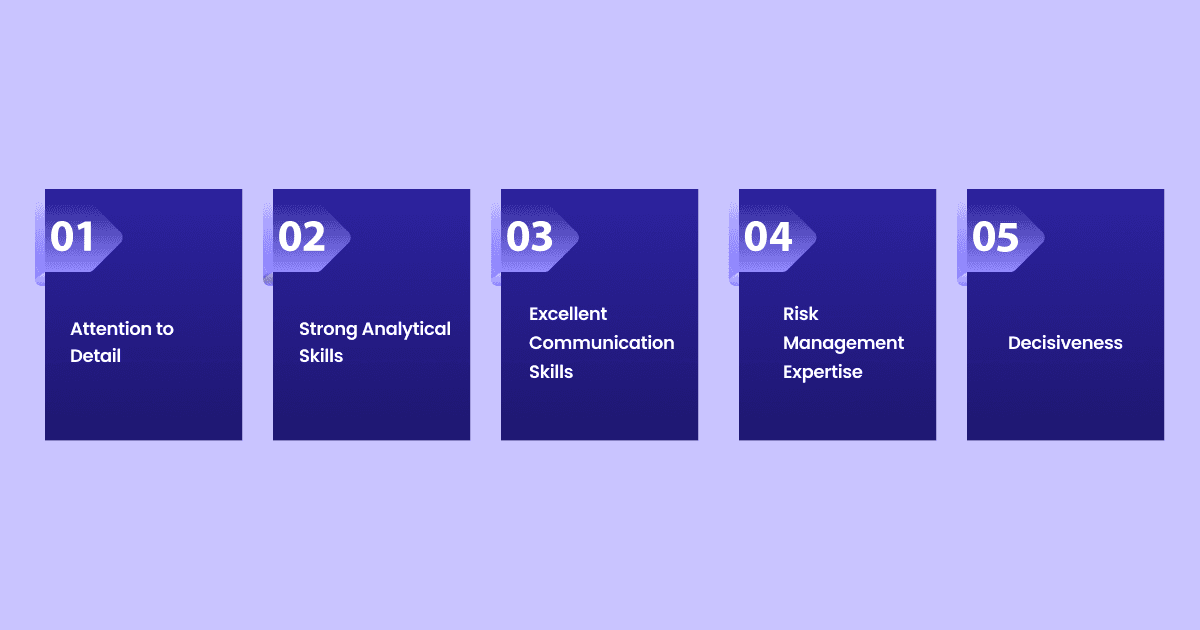

A high-performing credit manager is critical to the success of credit management. These individuals are responsible for overseeing credit policies, analyzing risk, and ensuring timely payments. Here are the key traits of an effective credit manager:

Attention to Detail: Successful credit managers pay close attention to the fine details of credit agreements, payment terms, and customer histories to ensure proper management.

Strong Analytical Skills: A good credit manager can analyze financial data, assess risk, and make strategic decisions based on the information available. Their ability to foresee potential issues before they arise is valuable.

Excellent Communication Skills: Credit managers must communicate effectively with both internal teams and customers. They should be able to negotiate terms, address concerns, and manage any disputes that arise professionally.

Risk Management Expertise: High-performing credit managers know how to assess and mitigate financial risks. They are skilled at identifying problem accounts early and taking corrective action.

Decisiveness and Leadership: A great credit manager makes timely and effective decisions. They lead by example, ensuring that the credit management team follows established procedures and maintains best practices.

What if you don’t need a credit manager when you can automate your workflow? With Rifa AI, simplify your credit risk assessments, collections, and compliance, all powered by cutting-edge automation. Automate 70% of your procedures, minimize human error and ensure real-time data accuracy.

Our advanced encryption safeguards sensitive financial data, and we comply with regulations like GDPR. Benefit from predictive analytics to optimize compliance and collections. Transform your processes, reduce costs, and achieve near-perfect accuracy in just days with Rifa AI.

Tips to Improve Your Credit Management Process

You can significantly enhance your cash flow, minimize bad debt, and foster stronger customer relationships by implementing strategic adjustments and utilizing modern tools. Let's explore actionable tips to elevate your credit management practices:

Establish Clear Credit Policies: A well-defined credit policy is key to reducing misunderstandings and ensuring consistency in decision-making. This policy should clearly outline the terms of credit, how you will collect payments, and what to do when payments are overdue.

Use Technology for Monitoring: Credit management tools and software can streamline the process, automate monitoring, and flag overdue payments, allowing you to act quickly and efficiently. Rifa AI can monitor customer accounts, flag overdue payments, and even automate follow-up communications, ensuring no account goes unnoticed.

Maintain Strong Customer Relationships: Open communication with customers is essential. Regularly checking in with customers about their payment schedules and offering flexible payment terms when needed can help prevent late payments. Rifa AI helps facilitate this by sending automated reminders through voice, chat and email, ensuring that your customers are always aware of payment deadlines.

With a solid understanding of the credit management process and its benefits, let’s now explore how AI automation can elevate your approach. It will make your business process even more efficient and strategic, particularly when it comes to managing late payments.

How AI Automation Can Help You Create a Strategic Credit Management Procedure for Late Payments

Artificial Intelligence (AI) and automation are revolutionizing credit management. Here’s how AI can simplify and enhance your credit management process:

Automates Key Aspects of Credit Management: AI can automate the review process, risk analysis, and collections, allowing you to efficiently manage customer credit accounts.

Real-Time Creditworthiness Assessment: AI-powered tools can assess a customer’s creditworthiness by analyzing vast amounts of data in real-time, helping you make informed decisions quickly.

Flagging Accounts at Risk of Late Payments: AI systems can automatically identify and flag accounts that are at risk of late payment, allowing you to take timely action.

Sending Automated Payment Reminders: AI tools can automatically send reminders to your customers about upcoming or overdue payments, reducing the possibility of missed payments.

Creating Custom Payment Plans: For overdue payments, AI can analyze a customer’s financial situation and suggest customized payment plans, improving the chances of recovering outstanding debts.

Reducing Human Error: Automating credit management minimizes the risk of human error, ensuring more accurate assessments and decisions.

Speeding Up the Process: AI accelerates the entire credit management process, enabling you to address overdue payments and credit issues faster.

Strategic Decision-Making: With AI, you can make more strategic and data-driven decisions, optimizing the credit management process and mitigating risks.

Incorporating AI into your credit management procedures can lead to better risk mitigation, fewer bad debts, and more efficient operations.

Conclusion

Credit management is a critical component of any financial operation for your business. By implementing effective credit management strategies, you can ensure timely payments, reduce bad debts, and maintain financial health.

With the right processes in place, along with modern tools such as AI automation, you can deal with the complexities of credit with greater ease. As you focus on improving your credit management practices, you’ll strengthen your financial position and set yourself up for long-term success.

Rifa AI offers an efficient, cost-effective, and personalized solution to streamline your collections and improve customer satisfaction. With real-time data processing, seamless omnichannel integration, and a fully compliant, automated system, Rifa AI is your trusted partner in debt recovery and other financial operations.

Mar 25, 2025

Mar 25, 2025

Mar 25, 2025

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved