Understanding Amortization Table and Schedule Basics

Understanding Amortization Table and Schedule Basics

Understanding Amortization Table and Schedule Basics

Understanding Amortization Table and Schedule Basics

Anant Sharma

Anant Sharma

Anant Sharma

Debt collection agencies are under increasing pressure as delinquency rates continue to rise. In Q3 2024, the mortgage delinquency rate for accounts overdue by 60 or more days rose to 1.22%, a 27-basis-point increase from 0.95% in Q2 2023.

Managing these delinquent accounts manually is becoming increasingly impractical, leading to inefficiencies that hinder recovery rates. Without a structured system, agencies risk missed follow-ups, compliance issues, and difficulties in prioritizing high-value accounts.

An amortization schedule is crucial in managing these accounts effectively. It provides a clear structure for tracking repayments, showing the breakdown of principal and interest, and helping agencies prioritize high-risk accounts. By using amortization schedules, agencies can stay on top of payments and forecast future collections.

In this blog, we'll explore how leveraging amortization schedules, alongside AI-driven automation, can streamline debt collection, improve recovery rates, and help agencies stay organized in a growingly complex industry.

What is an Amortization Schedule?

An amortization schedule is more than just a payment timeline—it is a strategic roadmap for debt collection agencies to track, analyze, and manage overdue accounts. It provides a clear structure of expected payments over time, breaking down each transaction into principal and interest, helping agencies maintain a precise record of outstanding balances.

By using an amortization schedule, debt collectors can pinpoint when payments are due, identify missed payments, and forecast future collections. This level of insight enables agencies to prioritize accounts that need immediate attention, optimize follow-up strategies, and improve recovery rates by acting at the right time.

With accurate tracking and structured insights, amortization schedules help agencies stay proactive rather than reactive, ensuring they can engage with debtors effectively, reduce delinquencies, and streamline the overall collection process.

Key Components of an Amortization Schedule

Knowing each element of this schedule provides valuable data that helps prioritize accounts, track overdue payments, and determine the best course of action for engaging with debtors.

The following key components of an amortization schedule enable agencies to refine their collection efforts and ensure maximum efficiency.

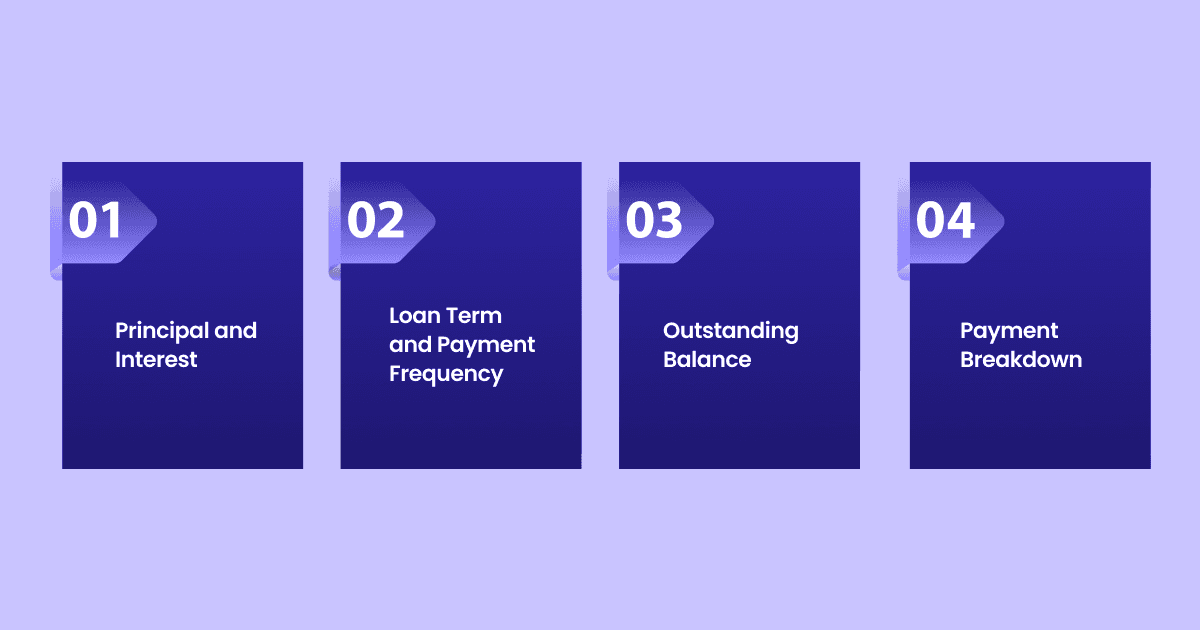

Principal and Interest

The principal is the original loan amount that remains unpaid, while interest is the cost charged for borrowing the money. For debt collection agencies, understanding these elements is crucial in assessing how much debt remains outstanding and how payments are structured.

For example, if a debtor has made payments primarily covering interest but little towards the principal, it indicates a slow repayment progress, signaling a need for more aggressive follow-up strategies.

Loan Term and Payment Frequency

The loan term and payment frequency provide insight into the duration and timing of repayments. Whether payments are made monthly, bi-weekly, or quarterly, collection agencies need to align their strategies accordingly.

For instance, if a loan has a long-term repayment schedule but the debtor has recently missed consecutive monthly payments, collectors can proactively intervene before the debt escalates into serious delinquency.

Outstanding Balance

Tracking the outstanding balance over time helps collection agencies determine the priority of accounts. Higher balances may require immediate attention to prevent further financial loss, while lower balances might be managed through automated follow-ups.

If a debtor’s remaining balance is significant and they have missed multiple payments, the agency might escalate the case to a more intensive collection process or negotiate a lump-sum settlement.

Payment Breakdown

An amortization schedule provides a detailed breakdown of each payment, showing how much goes toward principal reduction versus interest. This insight allows agencies to refine their collection strategies.

For example, if a debtor is only making minimum payments that barely reduce the principal, collectors can offer alternative payment plans that encourage faster debt reduction, improving the chances of full recovery.

By understanding these key components, debt collection agencies can make data-driven decisions, improve efficiency, and maximize recovery rates while maintaining compliance with regulations.

How Amortization Schedules Help Debt Collection Agencies Improve Collection Strategies?

Amortization schedules serve as a powerful tool for improving debt collection strategies. By offering visibility into missed payments, outstanding balances, and payment trends, they help agencies take a proactive approach to debt recovery.

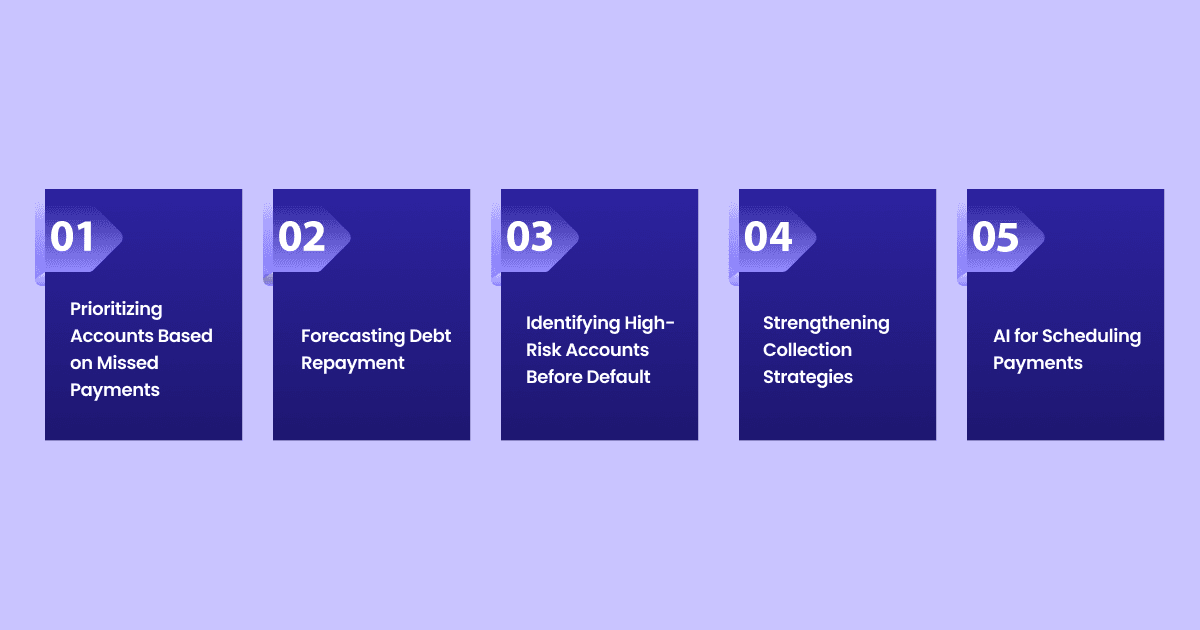

Prioritizing Accounts Based on Missed Payments

A structured schedule allows agencies to track when payments are due and identify missed payments in real time.

Example Amortization Schedule for John Miller

Payment Date | Payment Amount | Principal Paid | Interest Paid | Remaining Balance |

Jan 1, 2024 | $500 | $300 | $200 | $9,700 |

Feb 1, 2024 | $500 | $310 | $190 | $9,390 |

Mar 1, 2024 | $500 | $320 | $180 | $9,070 |

Apr 1, 2024 | $500 | $330 | $170 | $8,740 |

If John Miller misses his April 1, 2024, payment, it may indicate financial distress. If he continues to miss payments for three consecutive months, agencies can prioritize his account for immediate follow-up.

Rifa AI offers customized payment plans, automated reminders, and proactive settlement negotiations to help prevent debts from escalating. Start optimizing your collections today with AI-powered solutions.

Additionally, you can categorize delinquent accounts based on the severity of the situation, ensuring that high-risk cases like John's receive prompt attention.

Forecasting Debt Repayment and Escalation Strategies

Debt collectors can use amortization schedules to predict when an account is expected to be fully repaid. In John Miller’s case, if he was expected to pay off his balance within six months but has only paid 20% of the scheduled amount, this signals a high risk of delinquency.

Then your agency can then adjust its strategy by offering a lump-sum settlement at a reduced amount or restructuring his repayment plan to prevent the debt from escalating further.

For example, if John’s remaining balance is $8,740, and he has consistently missed payments, the agency might offer him a one-time settlement of $7,500 to close the account immediately. This approach helps recover funds while preventing further delinquency.

Identifying High-Risk Accounts Before Default

By tracking payment progress, agencies can detect patterns that indicate a debtor is at risk of default. If John Miller’s payments gradually decrease from $500 to $250, it may indicate financial struggles.

Early intervention—whether through reminders, restructuring options, or negotiation tactics—can increase the likelihood of recovery before the debt becomes irrecoverable.

For instance, if John contacts your agency stating that he can only afford $250 per month due to job loss, then you can proactively offer a modified repayment plan with reduced installments rather than letting the account default completely. This maintains a steady recovery flow while preventing legal actions or charge-offs.

Strengthening Collection Strategies with Behavioral Insights

Amortization schedules provide debt collection agencies with valuable insights into payment trends and debtor behaviors. By analyzing these trends, agencies can create customized recovery strategies for different debtor profiles. For example, if a significant portion of accounts show late payments at a certain period each month, the agency can adjust its reminder strategies to align with payday cycles, improving collection success rates.

Moreover, agencies can compare repayment behaviors across multiple accounts to identify broader trends, such as industries experiencing higher delinquency rates. This information allows agencies to refine their collection policies and allocate resources more effectively, ensuring optimal recovery performance.

By using amortization schedules effectively, debt collection agencies can improve efficiency, reduce delinquencies, and maximize recoveries while maintaining compliance and debtor engagement.

Benefits of Using AI for Scheduling Payments

AI is changing the way debt collection agencies operate, offering smarter, faster, and more effective solutions to maximize recoveries. While automation and cost reduction are significant advantages, AI brings a host of other benefits that enhance debtor engagement, risk management, and long-term financial stability.

Dynamic Payment Restructuring for At-Risk Debtors

Many debtors fail to pay on time due to financial hardship, not avoidance. Traditional collection strategies often apply a one-size-fits-all approach, leading to friction and higher default rates.

AI-driven debt collection tools analyze a debtor’s financial situation and payment history to suggest customized repayment plans that align with their ability to pay. By offering tailored restructuring options in real time, AI improves repayment rates while maintaining positive debtor relationships.

Rifa AI detects early signs of financial distress and proactively offers personalized payment plans, increasing voluntary repayments. Its AI voice agents guide debtors through flexible repayment options, reducing delinquency rates and improving overall recovery outcomes.

Multi-Channel Communication Strategies for Higher Response Rates

Debt collection is no longer just about phone calls. Many debtors prefer emails, text messages, or even WhatsApp reminders over direct calls. AI enables agencies to engage debtors through multiple channels, adjusting the approach based on individual preferences and response patterns.

By meeting debtors where they are most comfortable, AI increases the likelihood of successful interactions and payments.

With AI-driven omnichannel engagement, Rifa AI ensures that debtors receive timely reminders through SMS, email, or voice calls, improving response rates by 40%. By analyzing debtor behavior, Rifa AI automatically selects the best channel and timing for maximum effectiveness.

Emotional Intelligence & Sentiment Analysis in Conversations

Handling overdue payments requires more than just persistence—it requires emotional intelligence. AI-powered voice assistants can detect stress, frustration, or willingness to cooperate based on speech patterns and word choice.

This enables the system to adjust the conversation style dynamically, ensuring a professional yet empathetic approach that encourages repayment rather than resistance.

Rifa AI's advanced sentiment analysis tailors conversations in real-time, allowing AI voice agents to identify and de-escalate tense situations. By using a more human-like, understanding tone, Rifa AI improves debtor cooperation and increases repayment commitments by 35%.

Fraud Detection and Risk Mitigation

Fraudulent disputes and identity theft can complicate debt collection efforts. AI enhances security by detecting suspicious activity, such as repeated disputes on the same account, payment inconsistencies, or impersonation attempts.

AI-powered fraud detection tools flag high-risk cases early, preventing unnecessary losses and protecting agencies from compliance risks.

Rifa AI integrates fraud detection algorithms that analyze debtor behavior and flag potential risks. This helps agencies take preemptive action, reducing fraudulent disputes and chargebacks while ensuring 100% compliance with regulatory standards.

Proactive Late Payment Prediction and Intervention

Rather than waiting for missed payments, AI predicts which accounts are at risk of falling behind. By analyzing income trends, spending behaviors, and past payment inconsistencies, AI can identify high-risk accounts before they become delinquent.

Agencies can then intervene with targeted outreach or early repayment incentives to prevent escalation.

Rifa AI's predictive analytics help agencies identify at-risk accounts 30% earlier than traditional methods. With proactive engagement strategies, agencies can recover more debts before they reach a critical delinquency stage, improving overall financial stability.

Scalable Debt Collection Without Increased Overhead

As agencies grow, managing a larger volume of accounts becomes increasingly difficult. Scaling up traditionally requires hiring more agents, increasing operational costs.

AI eliminates this limitation by handling an unlimited number of calls, messages, and follow-ups simultaneously—without compromising quality or compliance.

With Rifa AI, agencies can automate up to 100,000 calls per day without hiring additional staff. This allows them to expand their operations 3x faster, without increasing overhead costs, making debt recovery more scalable and profitable.

From personalized repayment plans to fraud detection and predictive analytics, AI ensures that agencies recover debts more efficiently while improving debtor relationships and compliance.

Read more: Top Finance Automation Tools for 2025

How Rifa AI Enhances Amortization Schedule Management

Traditional debt collection methods are resource-heavy and inefficient, especially with rising missed payments. Rifa AI integrates with amortization schedules to automate key processes, boost recovery rates, and reduce operational costs.

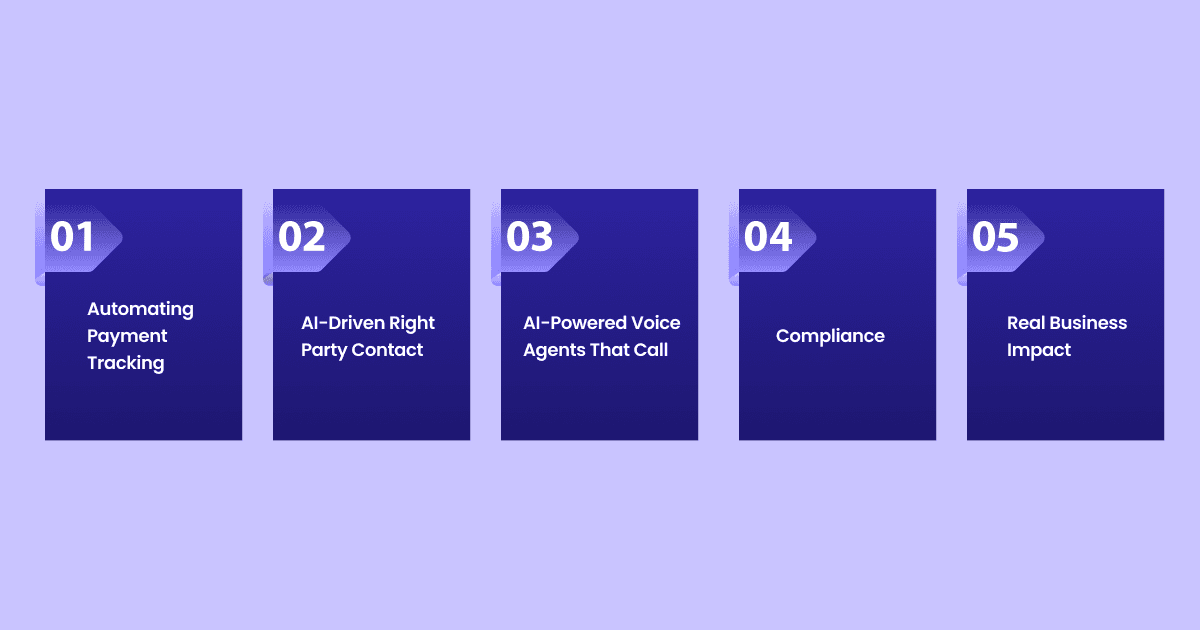

Automating Payment Tracking & Follow-Ups: Tracking payments and ensuring timely follow-ups can be time-consuming and error-prone. Rifa AI automates payment monitoring, analyzes debtor behavior, and sends personalized reminders via SMS, email, or calls based on responsiveness, ensuring no overdue account is missed.

AI-Driven Right Party Contact (RPC) Optimization: Rifa AI improves contact efficiency by analyzing debtor behavior and call history to reach the right individual at the right time, enhancing engagement. This results in higher contact rates (over 15%) and faster debt resolution.

AI-Powered Voice Agents That Call, Convert & Close: Rifa AI’s voice agents handle thousands of collection calls, offering payment reminders, answering queries, and negotiating settlements in real time. These AI-driven interactions mimic human conversations, improving efficiency and compliance.

Compliance & Secure Debt Recovery: Rifa AI ensures compliance with regulations like FDCPA and GDPR, providing secure automated solutions. With SOC 2 Type 1 & 2 certification, every interaction is logged and monitored, aiding in dispute resolution and legal compliance.

Real Business Impact: Measurable Results: Rifa AI boosts collection performance:

40% higher payment conversions with personalized calls

30% faster debt recovery through automated follow-ups

2x agent productivity by automating routine tasks

50% cost reduction through automation of routine calls

Simplify Debt Collection Amortization Schedule Management

Managing debt collection efficiently requires more than just tracking due dates—it demands intelligent insights, timely interventions, and strategic follow-ups. Agencies need a solution that not only monitors payments but also anticipates risks, identifies patterns, and ensures that debtors are engaged at the right moment.

AI-powered amortization management takes this process to the next level by enhancing accuracy, minimizing missed payments, and providing real-time insights that enable proactive debt recovery strategies.

Rifa AI transforms debt collection by integrating automation and intelligence into every stage of the process. With automated voice agents, real-time payment tracking, and predictive analytics, agencies can reduce manual effort while improving engagement rates. AI-powered systems ensure that every debtor interaction is optimized, whether through personalized reminders, strategic follow-ups, or escalations based on risk levels.

The result? A 40% increase in payment conversions, 30% faster debt recovery, and 50% cost savings—allowing agencies to maximize efficiency and revenue while reducing operational burdens.

See how AI-driven collections can work for you. Book a demo with Rifa AI today.

Debt collection agencies are under increasing pressure as delinquency rates continue to rise. In Q3 2024, the mortgage delinquency rate for accounts overdue by 60 or more days rose to 1.22%, a 27-basis-point increase from 0.95% in Q2 2023.

Managing these delinquent accounts manually is becoming increasingly impractical, leading to inefficiencies that hinder recovery rates. Without a structured system, agencies risk missed follow-ups, compliance issues, and difficulties in prioritizing high-value accounts.

An amortization schedule is crucial in managing these accounts effectively. It provides a clear structure for tracking repayments, showing the breakdown of principal and interest, and helping agencies prioritize high-risk accounts. By using amortization schedules, agencies can stay on top of payments and forecast future collections.

In this blog, we'll explore how leveraging amortization schedules, alongside AI-driven automation, can streamline debt collection, improve recovery rates, and help agencies stay organized in a growingly complex industry.

What is an Amortization Schedule?

An amortization schedule is more than just a payment timeline—it is a strategic roadmap for debt collection agencies to track, analyze, and manage overdue accounts. It provides a clear structure of expected payments over time, breaking down each transaction into principal and interest, helping agencies maintain a precise record of outstanding balances.

By using an amortization schedule, debt collectors can pinpoint when payments are due, identify missed payments, and forecast future collections. This level of insight enables agencies to prioritize accounts that need immediate attention, optimize follow-up strategies, and improve recovery rates by acting at the right time.

With accurate tracking and structured insights, amortization schedules help agencies stay proactive rather than reactive, ensuring they can engage with debtors effectively, reduce delinquencies, and streamline the overall collection process.

Key Components of an Amortization Schedule

Knowing each element of this schedule provides valuable data that helps prioritize accounts, track overdue payments, and determine the best course of action for engaging with debtors.

The following key components of an amortization schedule enable agencies to refine their collection efforts and ensure maximum efficiency.

Principal and Interest

The principal is the original loan amount that remains unpaid, while interest is the cost charged for borrowing the money. For debt collection agencies, understanding these elements is crucial in assessing how much debt remains outstanding and how payments are structured.

For example, if a debtor has made payments primarily covering interest but little towards the principal, it indicates a slow repayment progress, signaling a need for more aggressive follow-up strategies.

Loan Term and Payment Frequency

The loan term and payment frequency provide insight into the duration and timing of repayments. Whether payments are made monthly, bi-weekly, or quarterly, collection agencies need to align their strategies accordingly.

For instance, if a loan has a long-term repayment schedule but the debtor has recently missed consecutive monthly payments, collectors can proactively intervene before the debt escalates into serious delinquency.

Outstanding Balance

Tracking the outstanding balance over time helps collection agencies determine the priority of accounts. Higher balances may require immediate attention to prevent further financial loss, while lower balances might be managed through automated follow-ups.

If a debtor’s remaining balance is significant and they have missed multiple payments, the agency might escalate the case to a more intensive collection process or negotiate a lump-sum settlement.

Payment Breakdown

An amortization schedule provides a detailed breakdown of each payment, showing how much goes toward principal reduction versus interest. This insight allows agencies to refine their collection strategies.

For example, if a debtor is only making minimum payments that barely reduce the principal, collectors can offer alternative payment plans that encourage faster debt reduction, improving the chances of full recovery.

By understanding these key components, debt collection agencies can make data-driven decisions, improve efficiency, and maximize recovery rates while maintaining compliance with regulations.

How Amortization Schedules Help Debt Collection Agencies Improve Collection Strategies?

Amortization schedules serve as a powerful tool for improving debt collection strategies. By offering visibility into missed payments, outstanding balances, and payment trends, they help agencies take a proactive approach to debt recovery.

Prioritizing Accounts Based on Missed Payments

A structured schedule allows agencies to track when payments are due and identify missed payments in real time.

Example Amortization Schedule for John Miller

Payment Date | Payment Amount | Principal Paid | Interest Paid | Remaining Balance |

Jan 1, 2024 | $500 | $300 | $200 | $9,700 |

Feb 1, 2024 | $500 | $310 | $190 | $9,390 |

Mar 1, 2024 | $500 | $320 | $180 | $9,070 |

Apr 1, 2024 | $500 | $330 | $170 | $8,740 |

If John Miller misses his April 1, 2024, payment, it may indicate financial distress. If he continues to miss payments for three consecutive months, agencies can prioritize his account for immediate follow-up.

Rifa AI offers customized payment plans, automated reminders, and proactive settlement negotiations to help prevent debts from escalating. Start optimizing your collections today with AI-powered solutions.

Additionally, you can categorize delinquent accounts based on the severity of the situation, ensuring that high-risk cases like John's receive prompt attention.

Forecasting Debt Repayment and Escalation Strategies

Debt collectors can use amortization schedules to predict when an account is expected to be fully repaid. In John Miller’s case, if he was expected to pay off his balance within six months but has only paid 20% of the scheduled amount, this signals a high risk of delinquency.

Then your agency can then adjust its strategy by offering a lump-sum settlement at a reduced amount or restructuring his repayment plan to prevent the debt from escalating further.

For example, if John’s remaining balance is $8,740, and he has consistently missed payments, the agency might offer him a one-time settlement of $7,500 to close the account immediately. This approach helps recover funds while preventing further delinquency.

Identifying High-Risk Accounts Before Default

By tracking payment progress, agencies can detect patterns that indicate a debtor is at risk of default. If John Miller’s payments gradually decrease from $500 to $250, it may indicate financial struggles.

Early intervention—whether through reminders, restructuring options, or negotiation tactics—can increase the likelihood of recovery before the debt becomes irrecoverable.

For instance, if John contacts your agency stating that he can only afford $250 per month due to job loss, then you can proactively offer a modified repayment plan with reduced installments rather than letting the account default completely. This maintains a steady recovery flow while preventing legal actions or charge-offs.

Strengthening Collection Strategies with Behavioral Insights

Amortization schedules provide debt collection agencies with valuable insights into payment trends and debtor behaviors. By analyzing these trends, agencies can create customized recovery strategies for different debtor profiles. For example, if a significant portion of accounts show late payments at a certain period each month, the agency can adjust its reminder strategies to align with payday cycles, improving collection success rates.

Moreover, agencies can compare repayment behaviors across multiple accounts to identify broader trends, such as industries experiencing higher delinquency rates. This information allows agencies to refine their collection policies and allocate resources more effectively, ensuring optimal recovery performance.

By using amortization schedules effectively, debt collection agencies can improve efficiency, reduce delinquencies, and maximize recoveries while maintaining compliance and debtor engagement.

Benefits of Using AI for Scheduling Payments

AI is changing the way debt collection agencies operate, offering smarter, faster, and more effective solutions to maximize recoveries. While automation and cost reduction are significant advantages, AI brings a host of other benefits that enhance debtor engagement, risk management, and long-term financial stability.

Dynamic Payment Restructuring for At-Risk Debtors

Many debtors fail to pay on time due to financial hardship, not avoidance. Traditional collection strategies often apply a one-size-fits-all approach, leading to friction and higher default rates.

AI-driven debt collection tools analyze a debtor’s financial situation and payment history to suggest customized repayment plans that align with their ability to pay. By offering tailored restructuring options in real time, AI improves repayment rates while maintaining positive debtor relationships.

Rifa AI detects early signs of financial distress and proactively offers personalized payment plans, increasing voluntary repayments. Its AI voice agents guide debtors through flexible repayment options, reducing delinquency rates and improving overall recovery outcomes.

Multi-Channel Communication Strategies for Higher Response Rates

Debt collection is no longer just about phone calls. Many debtors prefer emails, text messages, or even WhatsApp reminders over direct calls. AI enables agencies to engage debtors through multiple channels, adjusting the approach based on individual preferences and response patterns.

By meeting debtors where they are most comfortable, AI increases the likelihood of successful interactions and payments.

With AI-driven omnichannel engagement, Rifa AI ensures that debtors receive timely reminders through SMS, email, or voice calls, improving response rates by 40%. By analyzing debtor behavior, Rifa AI automatically selects the best channel and timing for maximum effectiveness.

Emotional Intelligence & Sentiment Analysis in Conversations

Handling overdue payments requires more than just persistence—it requires emotional intelligence. AI-powered voice assistants can detect stress, frustration, or willingness to cooperate based on speech patterns and word choice.

This enables the system to adjust the conversation style dynamically, ensuring a professional yet empathetic approach that encourages repayment rather than resistance.

Rifa AI's advanced sentiment analysis tailors conversations in real-time, allowing AI voice agents to identify and de-escalate tense situations. By using a more human-like, understanding tone, Rifa AI improves debtor cooperation and increases repayment commitments by 35%.

Fraud Detection and Risk Mitigation

Fraudulent disputes and identity theft can complicate debt collection efforts. AI enhances security by detecting suspicious activity, such as repeated disputes on the same account, payment inconsistencies, or impersonation attempts.

AI-powered fraud detection tools flag high-risk cases early, preventing unnecessary losses and protecting agencies from compliance risks.

Rifa AI integrates fraud detection algorithms that analyze debtor behavior and flag potential risks. This helps agencies take preemptive action, reducing fraudulent disputes and chargebacks while ensuring 100% compliance with regulatory standards.

Proactive Late Payment Prediction and Intervention

Rather than waiting for missed payments, AI predicts which accounts are at risk of falling behind. By analyzing income trends, spending behaviors, and past payment inconsistencies, AI can identify high-risk accounts before they become delinquent.

Agencies can then intervene with targeted outreach or early repayment incentives to prevent escalation.

Rifa AI's predictive analytics help agencies identify at-risk accounts 30% earlier than traditional methods. With proactive engagement strategies, agencies can recover more debts before they reach a critical delinquency stage, improving overall financial stability.

Scalable Debt Collection Without Increased Overhead

As agencies grow, managing a larger volume of accounts becomes increasingly difficult. Scaling up traditionally requires hiring more agents, increasing operational costs.

AI eliminates this limitation by handling an unlimited number of calls, messages, and follow-ups simultaneously—without compromising quality or compliance.

With Rifa AI, agencies can automate up to 100,000 calls per day without hiring additional staff. This allows them to expand their operations 3x faster, without increasing overhead costs, making debt recovery more scalable and profitable.

From personalized repayment plans to fraud detection and predictive analytics, AI ensures that agencies recover debts more efficiently while improving debtor relationships and compliance.

Read more: Top Finance Automation Tools for 2025

How Rifa AI Enhances Amortization Schedule Management

Traditional debt collection methods are resource-heavy and inefficient, especially with rising missed payments. Rifa AI integrates with amortization schedules to automate key processes, boost recovery rates, and reduce operational costs.

Automating Payment Tracking & Follow-Ups: Tracking payments and ensuring timely follow-ups can be time-consuming and error-prone. Rifa AI automates payment monitoring, analyzes debtor behavior, and sends personalized reminders via SMS, email, or calls based on responsiveness, ensuring no overdue account is missed.

AI-Driven Right Party Contact (RPC) Optimization: Rifa AI improves contact efficiency by analyzing debtor behavior and call history to reach the right individual at the right time, enhancing engagement. This results in higher contact rates (over 15%) and faster debt resolution.

AI-Powered Voice Agents That Call, Convert & Close: Rifa AI’s voice agents handle thousands of collection calls, offering payment reminders, answering queries, and negotiating settlements in real time. These AI-driven interactions mimic human conversations, improving efficiency and compliance.

Compliance & Secure Debt Recovery: Rifa AI ensures compliance with regulations like FDCPA and GDPR, providing secure automated solutions. With SOC 2 Type 1 & 2 certification, every interaction is logged and monitored, aiding in dispute resolution and legal compliance.

Real Business Impact: Measurable Results: Rifa AI boosts collection performance:

40% higher payment conversions with personalized calls

30% faster debt recovery through automated follow-ups

2x agent productivity by automating routine tasks

50% cost reduction through automation of routine calls

Simplify Debt Collection Amortization Schedule Management

Managing debt collection efficiently requires more than just tracking due dates—it demands intelligent insights, timely interventions, and strategic follow-ups. Agencies need a solution that not only monitors payments but also anticipates risks, identifies patterns, and ensures that debtors are engaged at the right moment.

AI-powered amortization management takes this process to the next level by enhancing accuracy, minimizing missed payments, and providing real-time insights that enable proactive debt recovery strategies.

Rifa AI transforms debt collection by integrating automation and intelligence into every stage of the process. With automated voice agents, real-time payment tracking, and predictive analytics, agencies can reduce manual effort while improving engagement rates. AI-powered systems ensure that every debtor interaction is optimized, whether through personalized reminders, strategic follow-ups, or escalations based on risk levels.

The result? A 40% increase in payment conversions, 30% faster debt recovery, and 50% cost savings—allowing agencies to maximize efficiency and revenue while reducing operational burdens.

See how AI-driven collections can work for you. Book a demo with Rifa AI today.

Mar 28, 2025

Mar 28, 2025

Mar 28, 2025

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved

Automate repetitive tasks to accelerate your growth

Copyright © 2025 Rifa AI

All Rights Reserved